Pimco warns Iran war could lead Federal Reserve to raise rates

For the better part of two years, markets have been pricing in a slow, steady descent in interest rates. Pimco, the world’s largest active bond manager, is now suggesting that trajectory might be about to reverse, and the catalyst isn’t domestic inflation data or a hot jobs report. It’s war.

Pacific Investment Management Company has warned that the ongoing conflict involving Iran could push the Federal Reserve toward raising interest rates rather than cutting them. The logic is straightforward: prolonged military conflict disrupts energy markets, energy disruptions drive up costs across the economy, and the Fed’s primary tool for fighting inflation is higher rates.

A divided Fed signals uncertainty

The Federal Open Market Committee held rates steady at 3.50%-3.75% during its April 29 meeting. That decision, on its own, was unsurprising.

What was surprising: the vote was 8-4. That level of dissent is unusual and worth paying attention to.

The four dissenters didn’t necessarily want an immediate hike. But they pushed for a clearer signal that rate increases are on the table, not just cuts. The dissenters emphasized that hikes are as plausible as cuts depending on how economic conditions evolve.

Energy shocks and the inflation problem

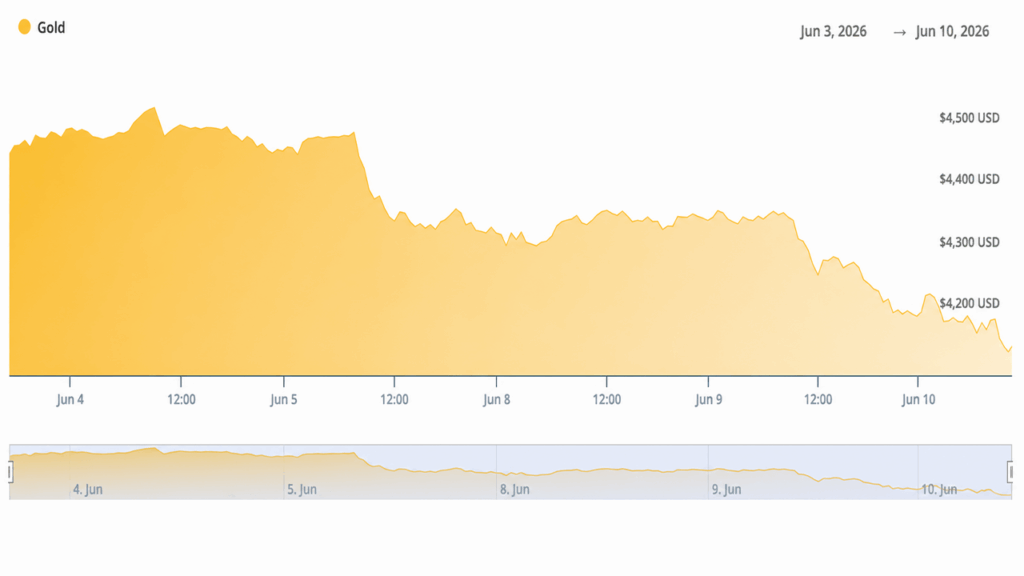

Pimco’s core concern centers on energy supply shocks. If Iranian oil exports get disrupted or Middle Eastern shipping routes become unreliable for an extended period, crude prices spike. Pimco warned that a prolonged conflict could lead to sustained energy supply shocks with profound global economic effects.

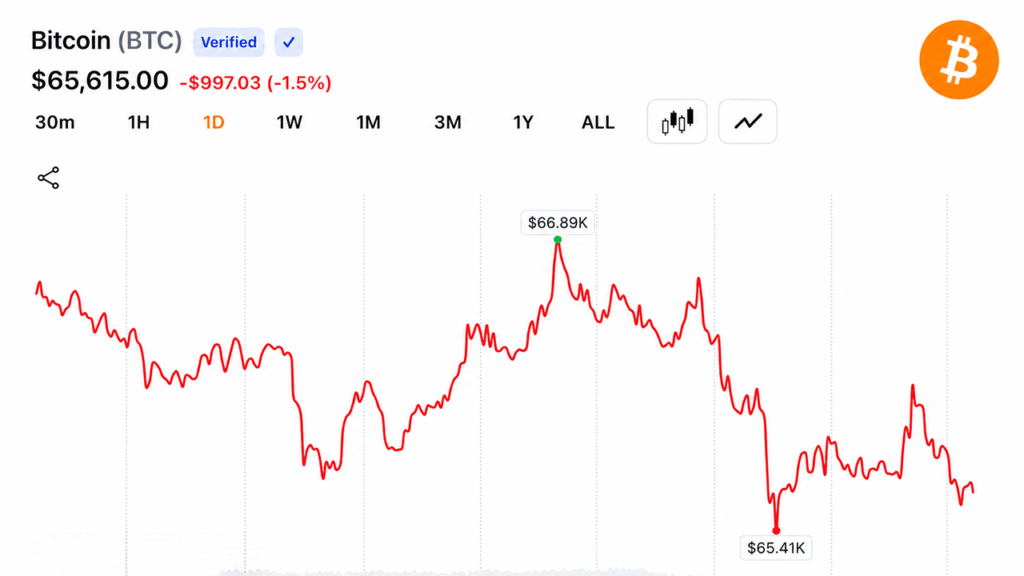

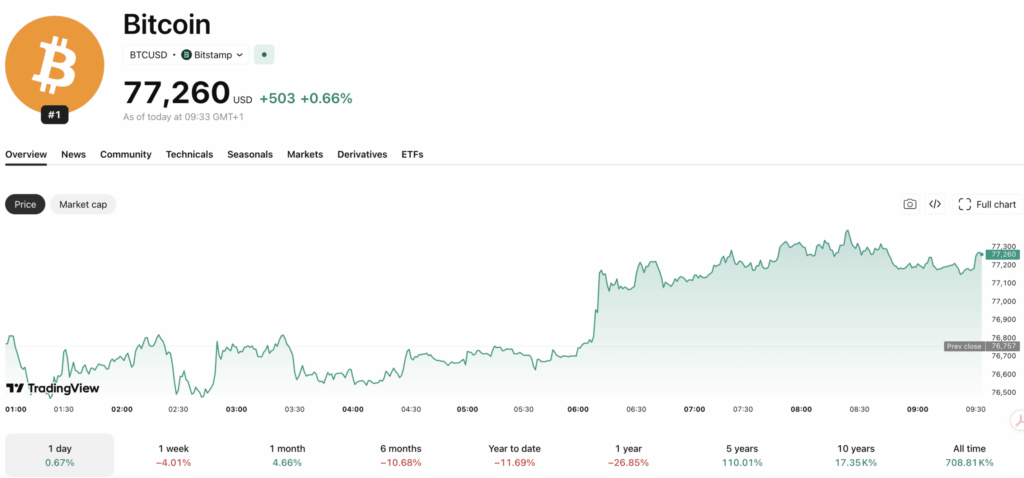

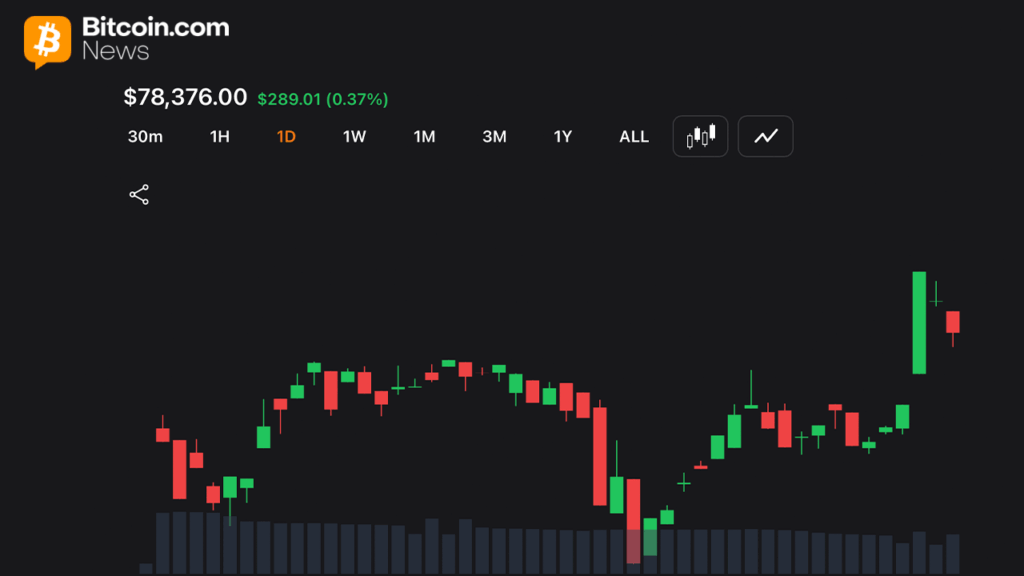

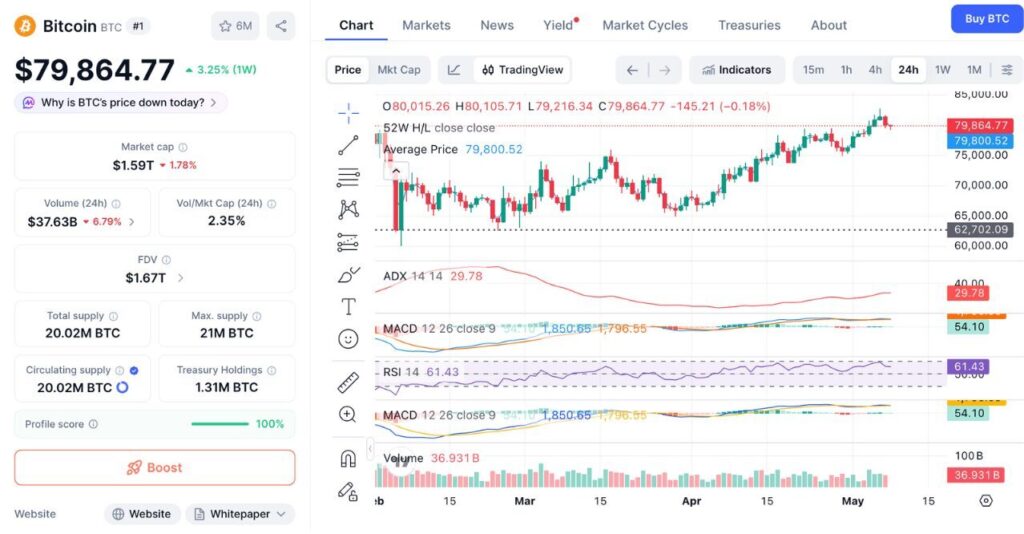

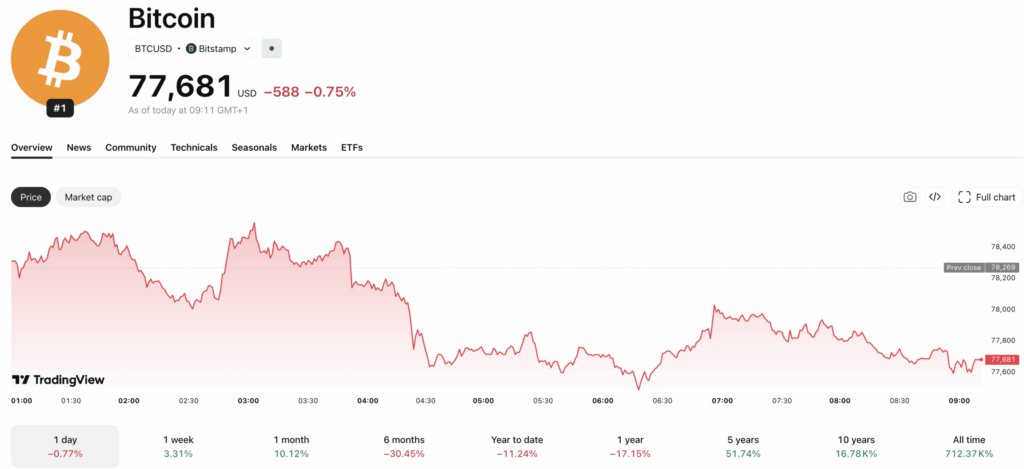

Treasury markets are already reacting. Two-year yields rose by 10 basis points to 3.48% following the escalation in conflict, while 10-year yields climbed to 4.03%. Traders have also started reducing expectations of rate cuts in 2026, with higher chances of hikes being priced into future central bank meetings.

What this means for investors

The bond market is arguably the most immediate place to watch. Rising yields on both the short and long end of the curve suggest investors are demanding more compensation for holding US government debt. Pimco itself, as the world’s premier bond shop, is presumably positioning accordingly.

Investors should watch the spread between two-year and 10-year Treasury yields closely. The current gap, with two-year yields at 3.48% and 10-year yields at 4.03%, shows a normally sloped curve. But if short-term yields start climbing faster than long-term yields, it would signal that markets expect the Fed to act aggressively on near-term inflation even at the risk of slowing the economy.

Disclosure: This article was edited by Editorial Team. For more information on how we create and review content, see our Editorial Policy.