What Can’t Be Seen, Can’t Be Seized

- Key Takeaways.

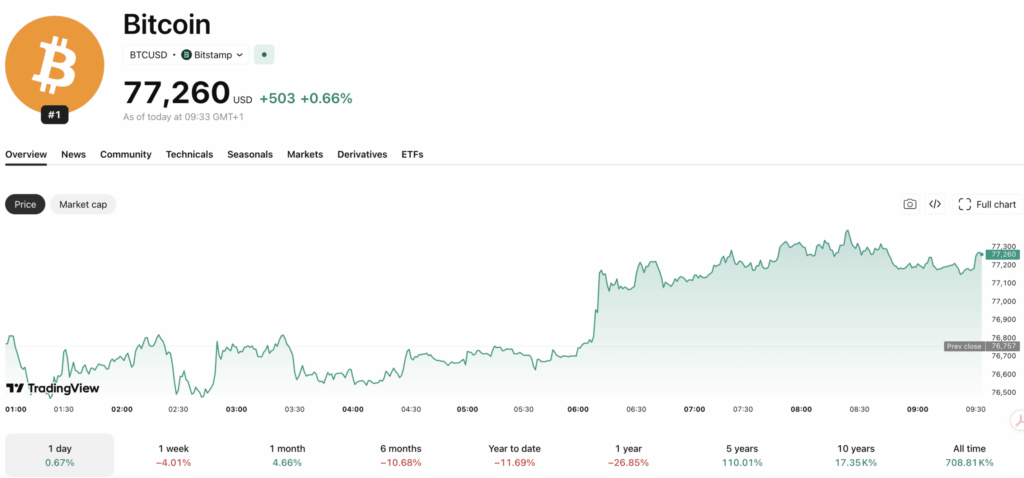

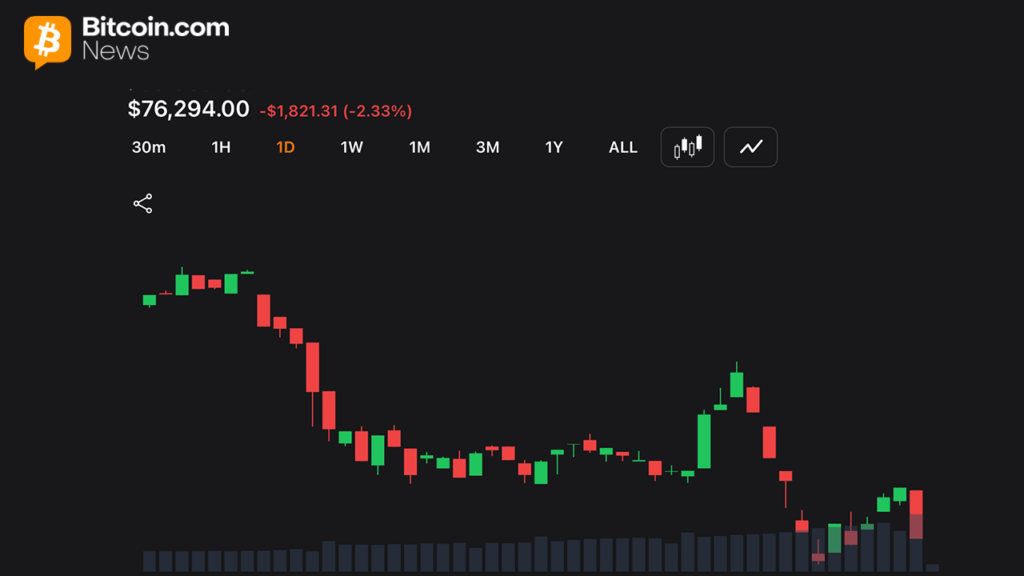

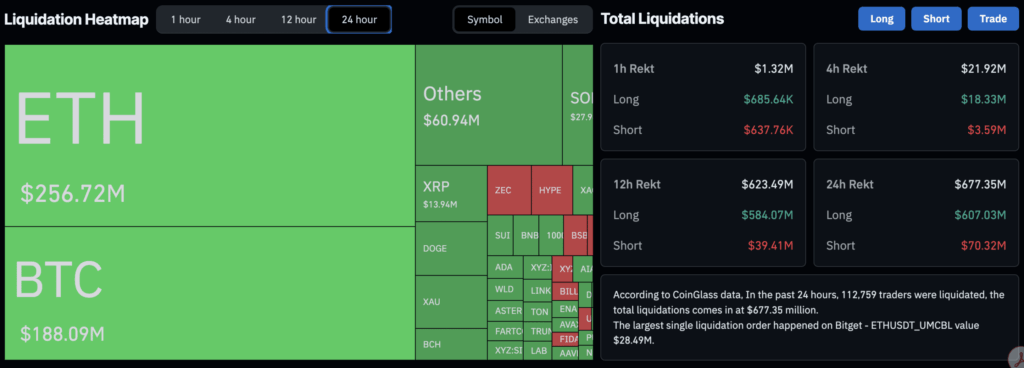

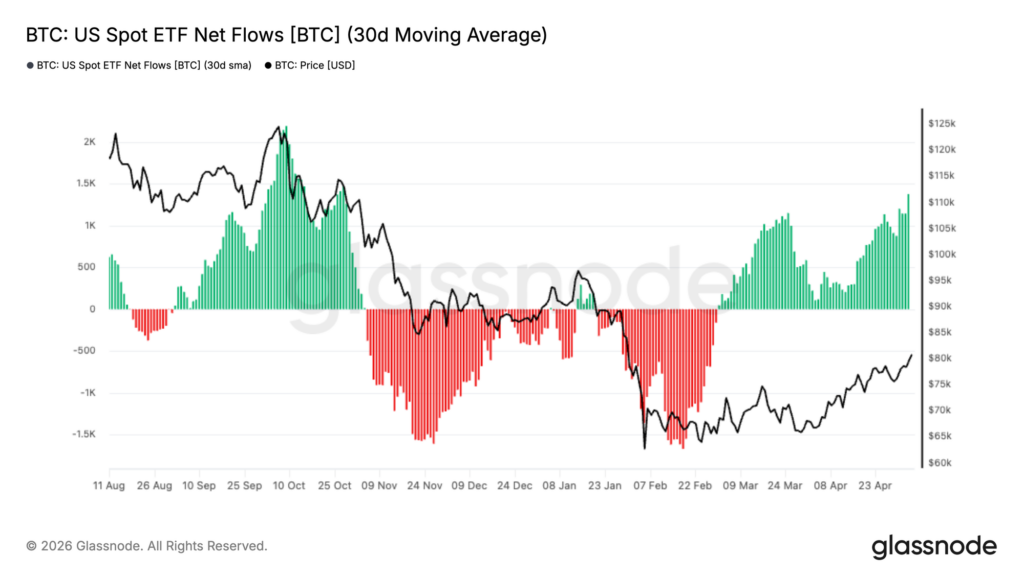

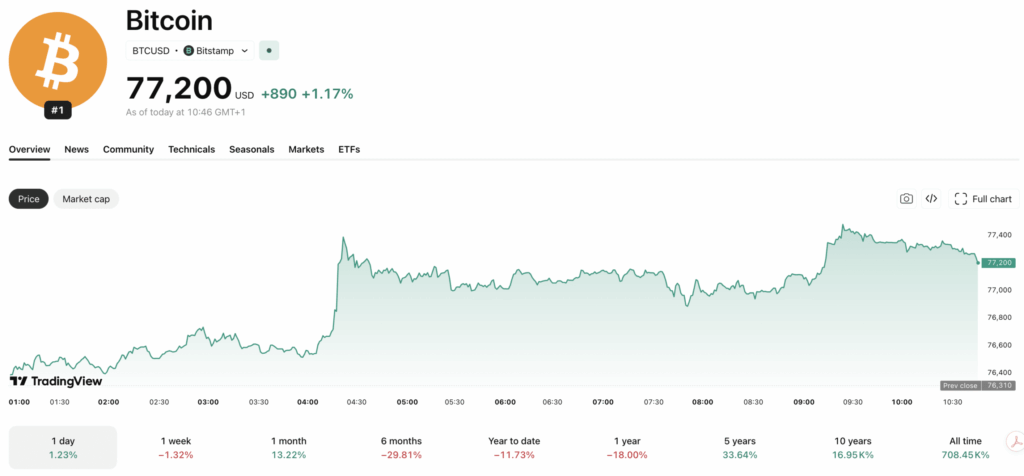

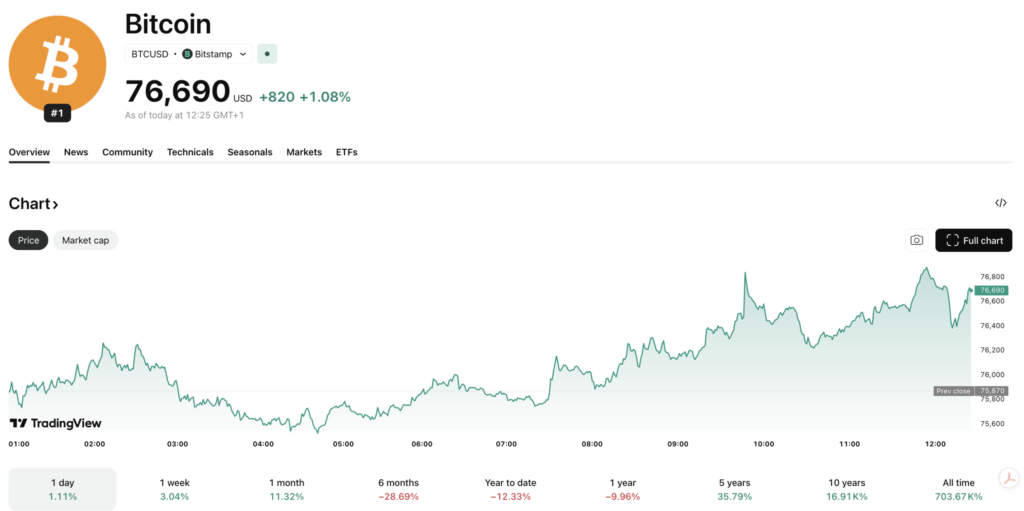

- Bitcoin held $80K as Jamie Coutts flagged treasury demand, pointing to a stronger next BTC bid.

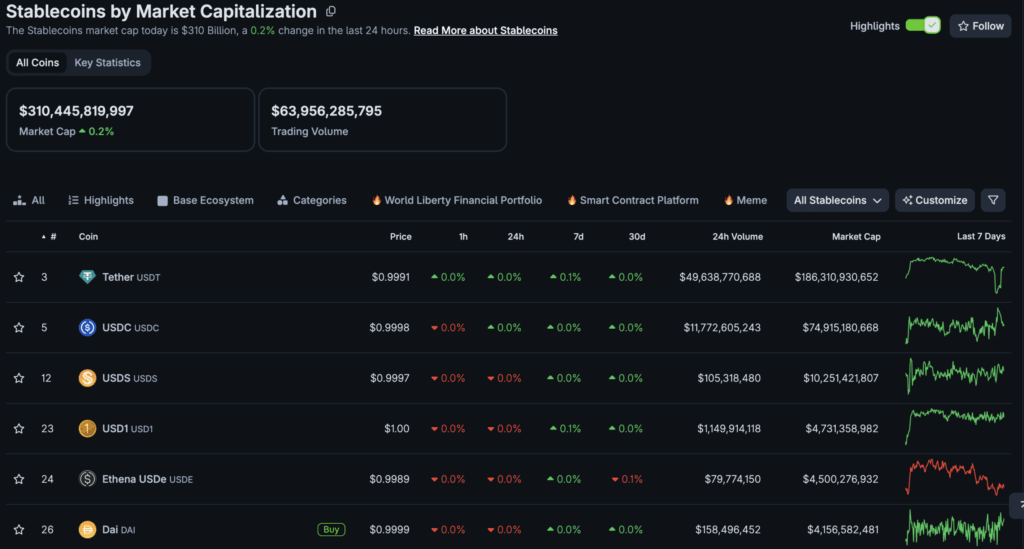

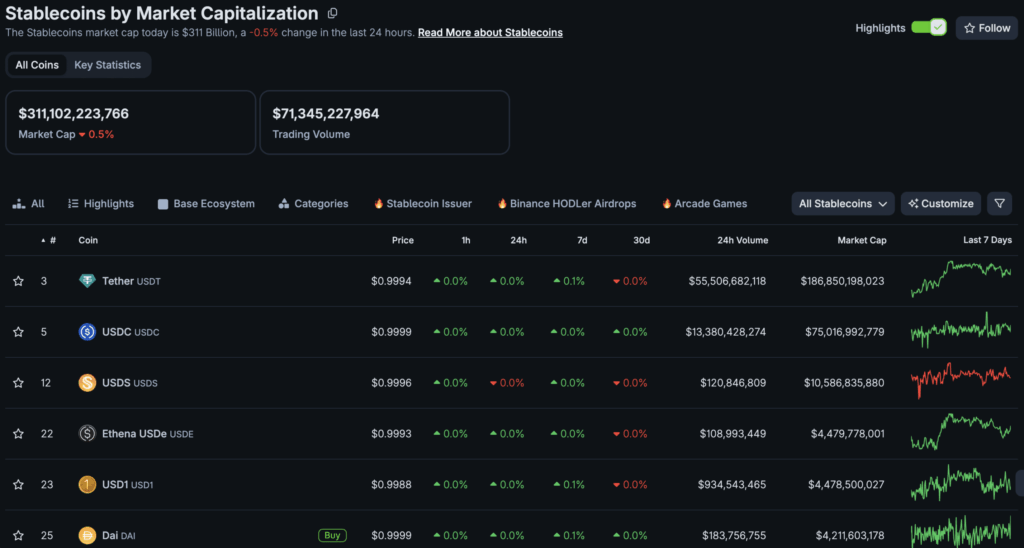

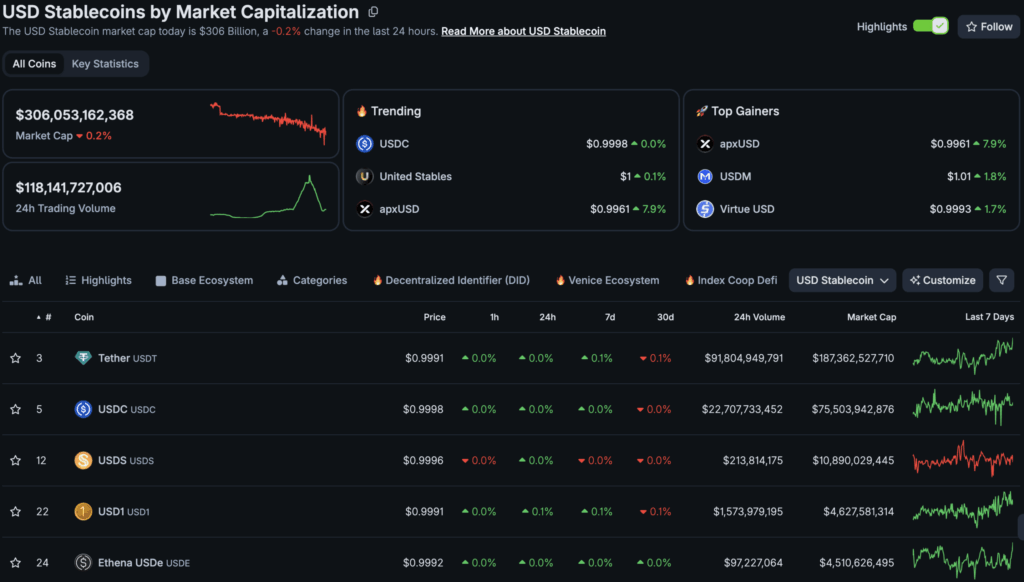

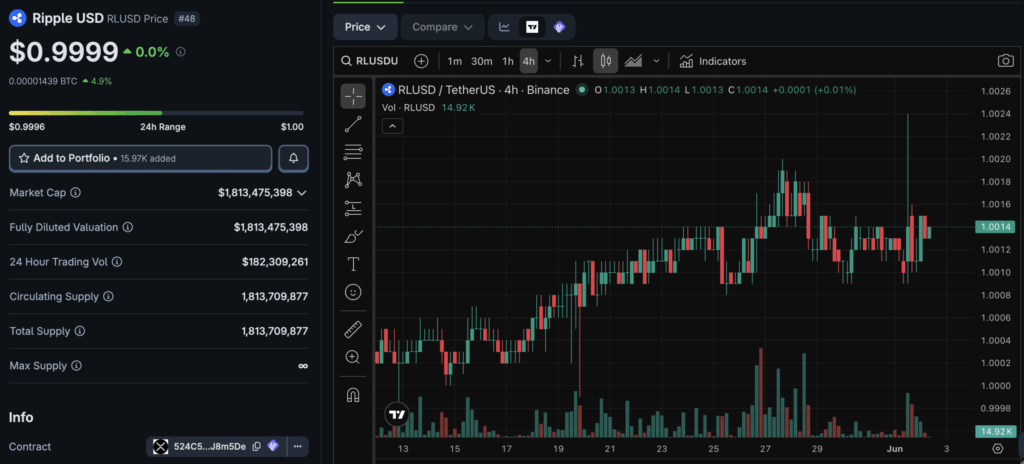

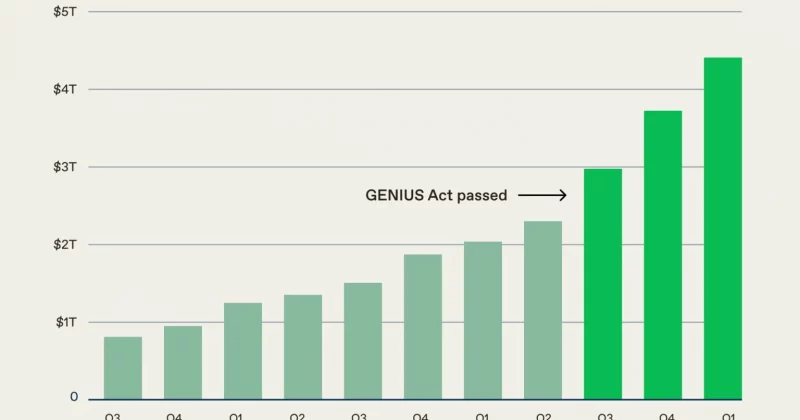

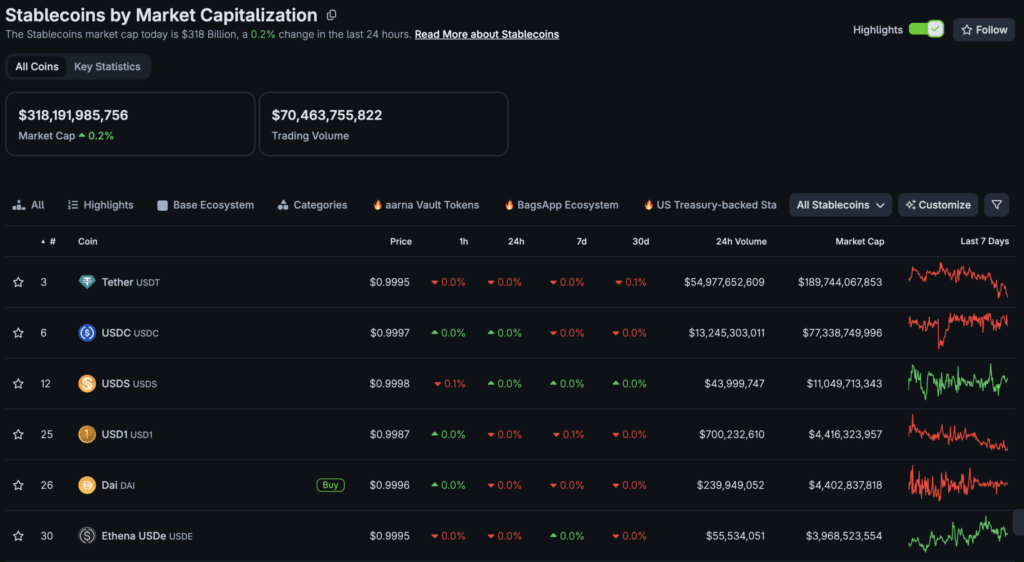

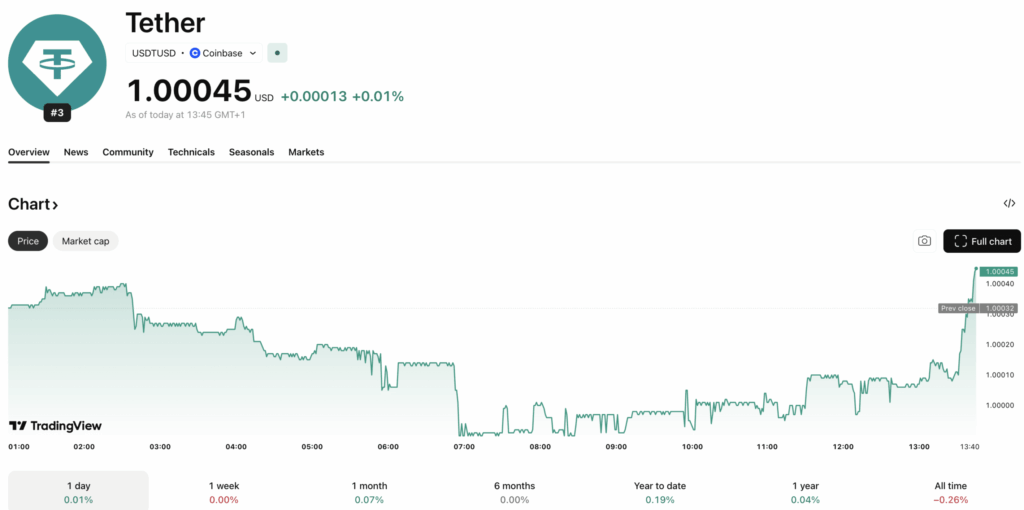

- Stablecoins hit $321B as Tether’s $20B gold stash and Kraken’s $600M deal pushed rails mainstream.

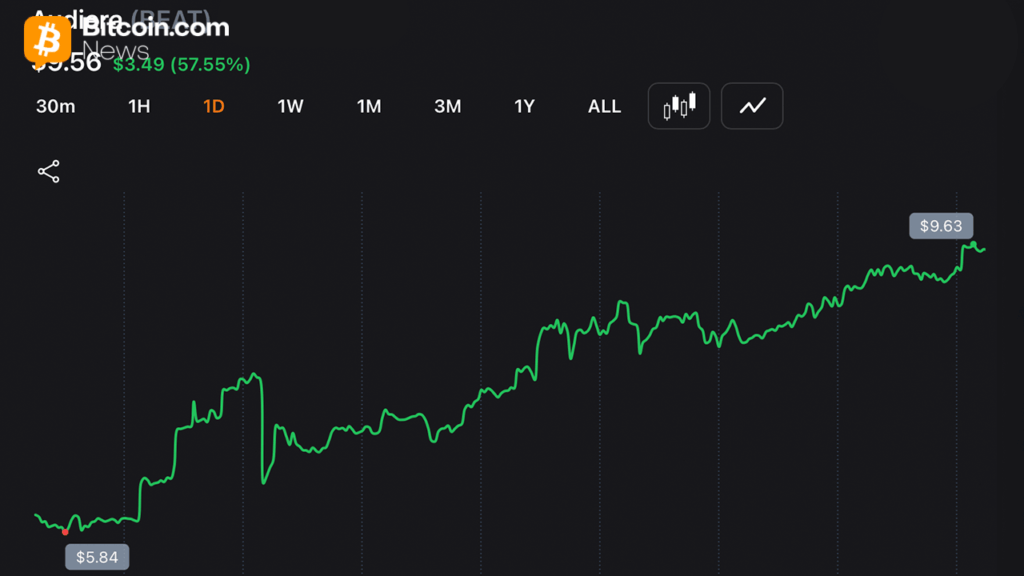

- Zcash rose 72% in 30 days as Tushar Jain backed privacy, setting up a bigger 2026 ZEC debate.

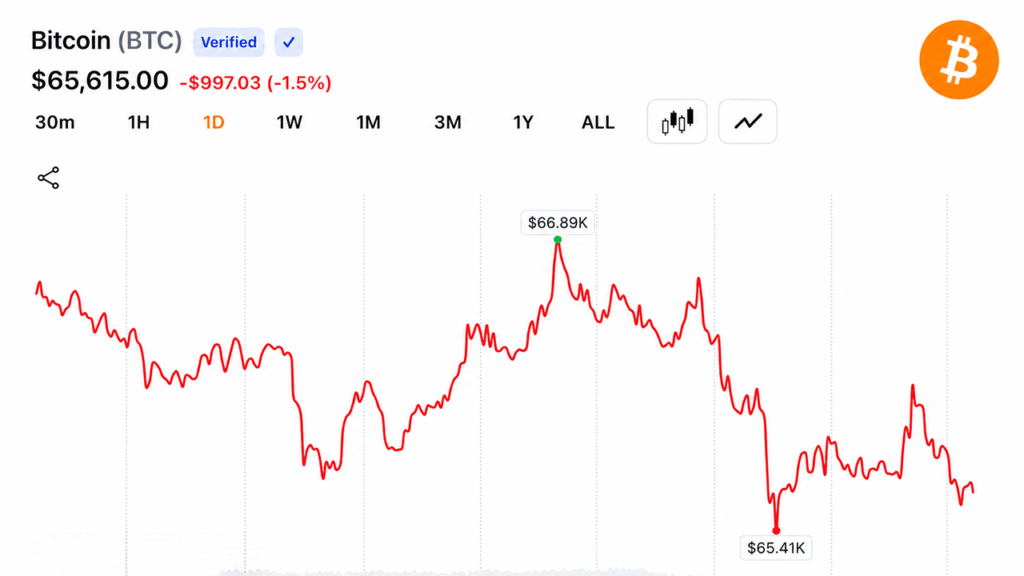

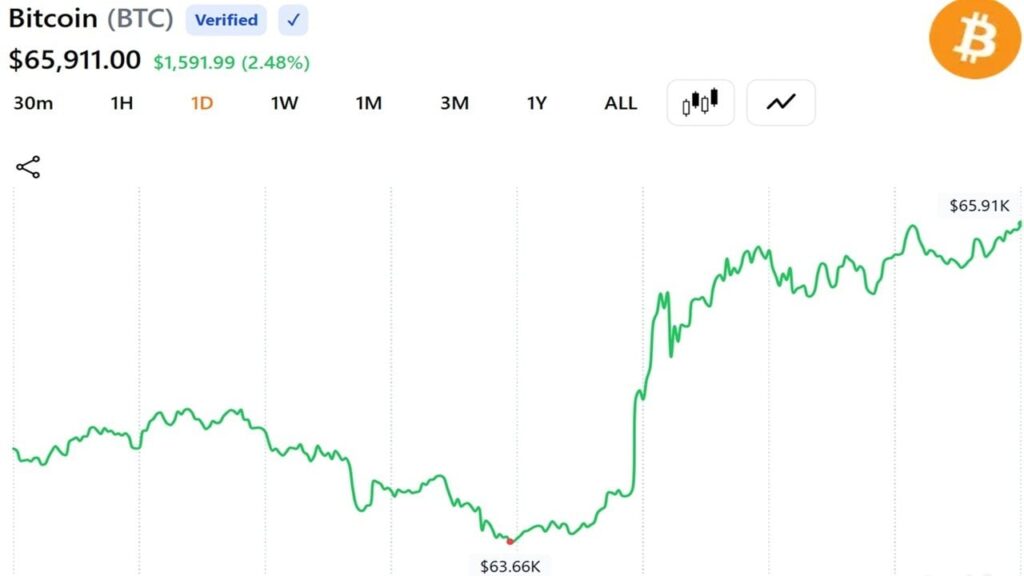

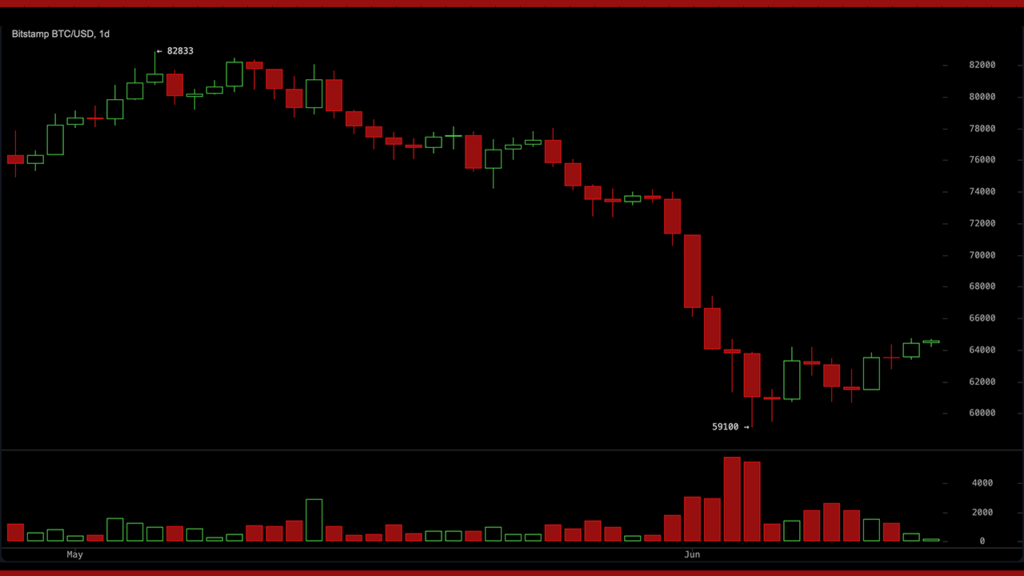

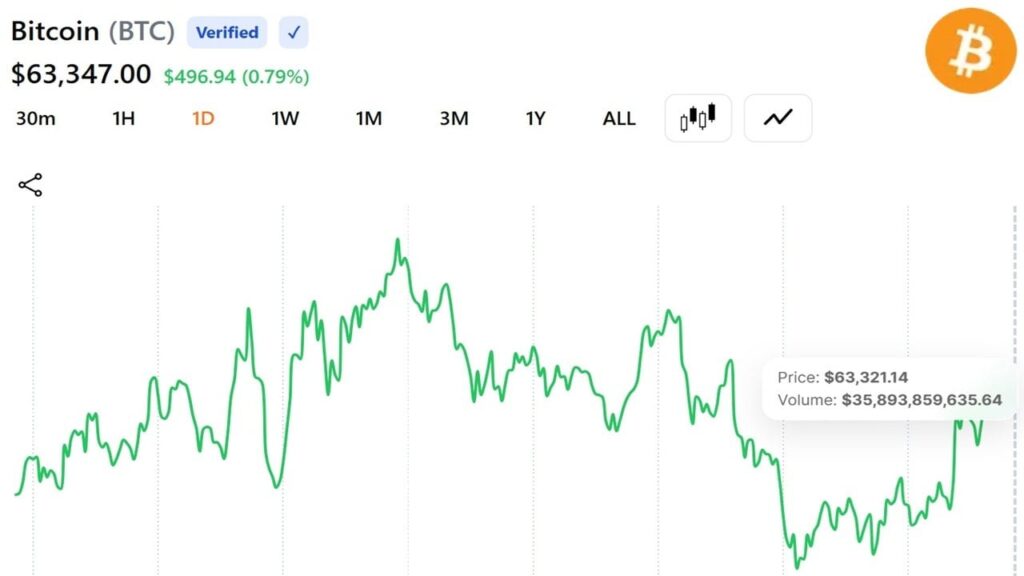

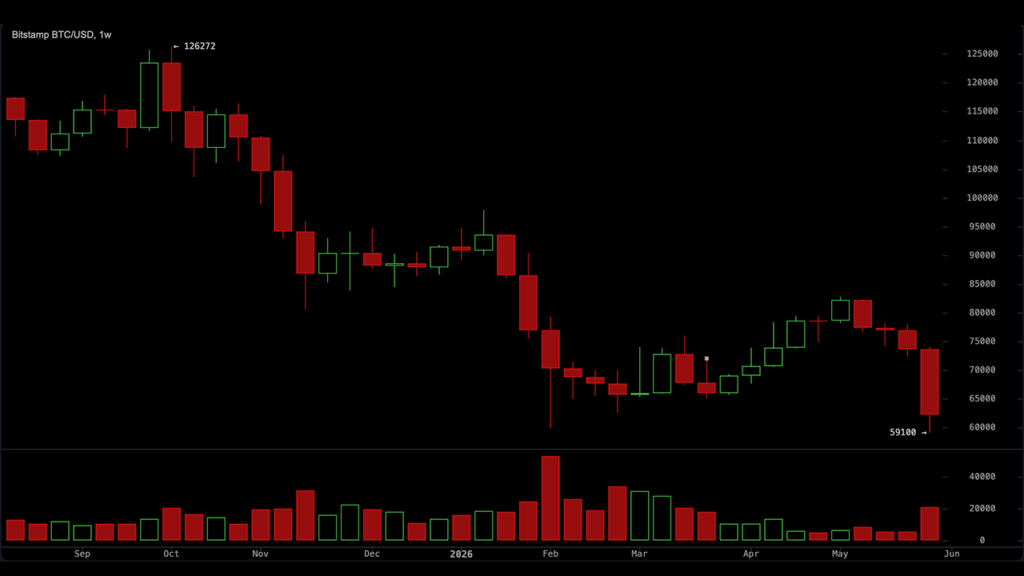

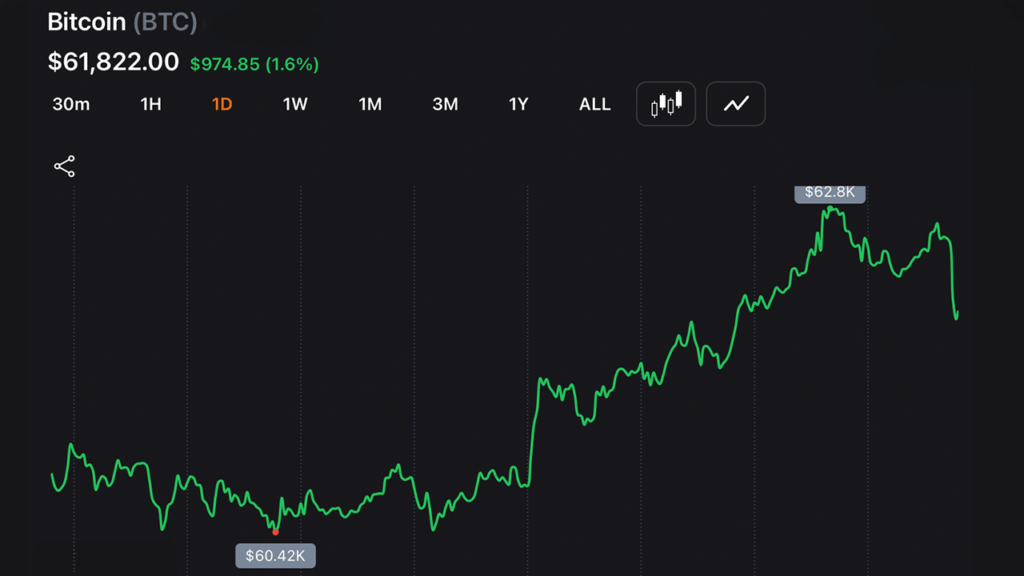

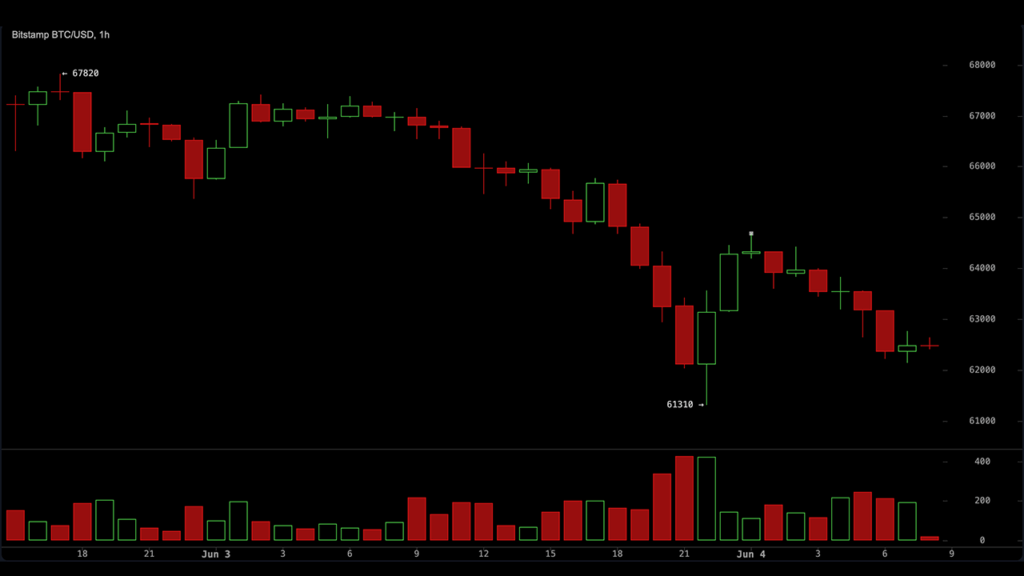

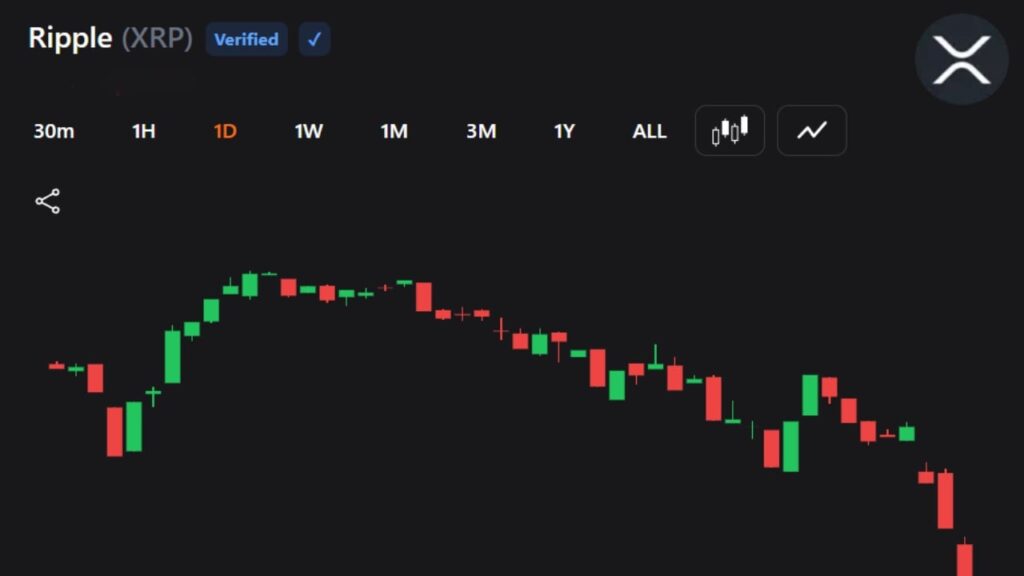

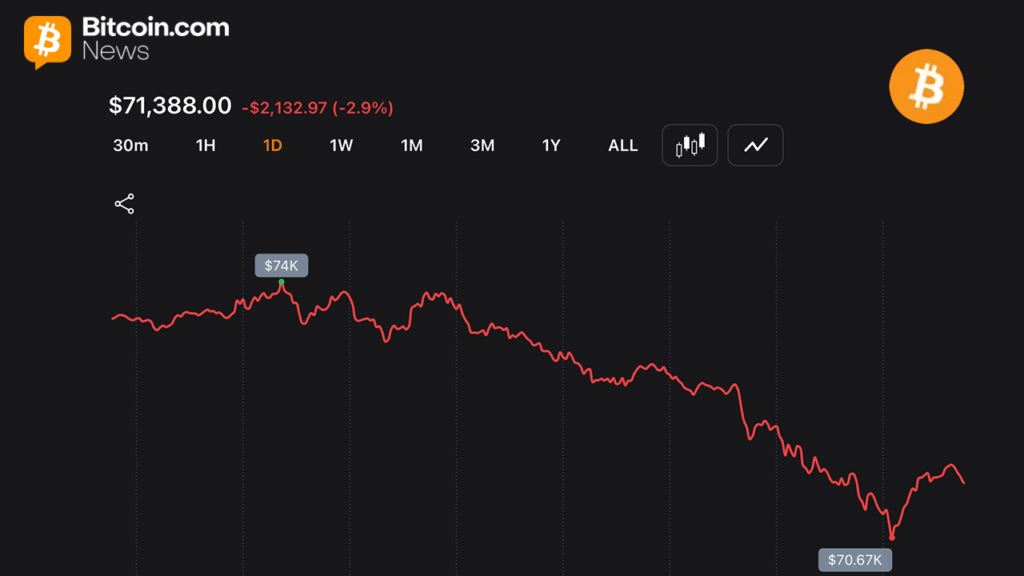

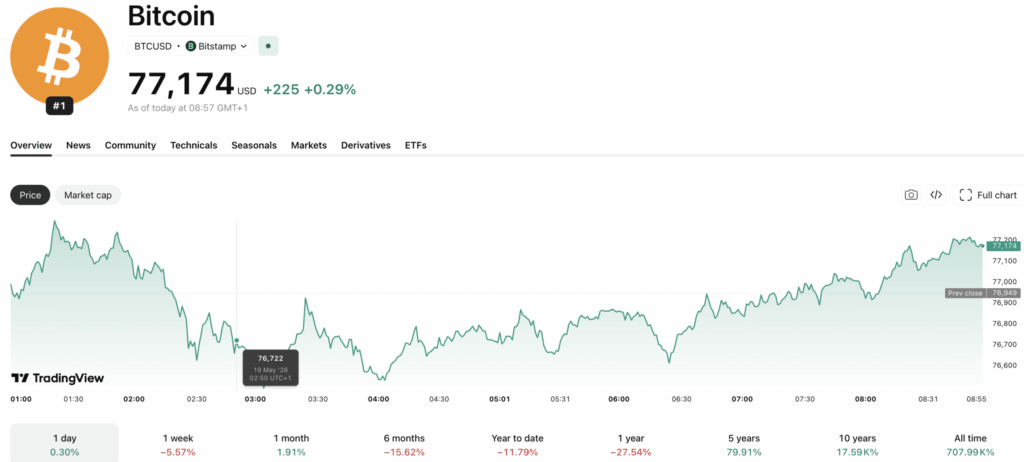

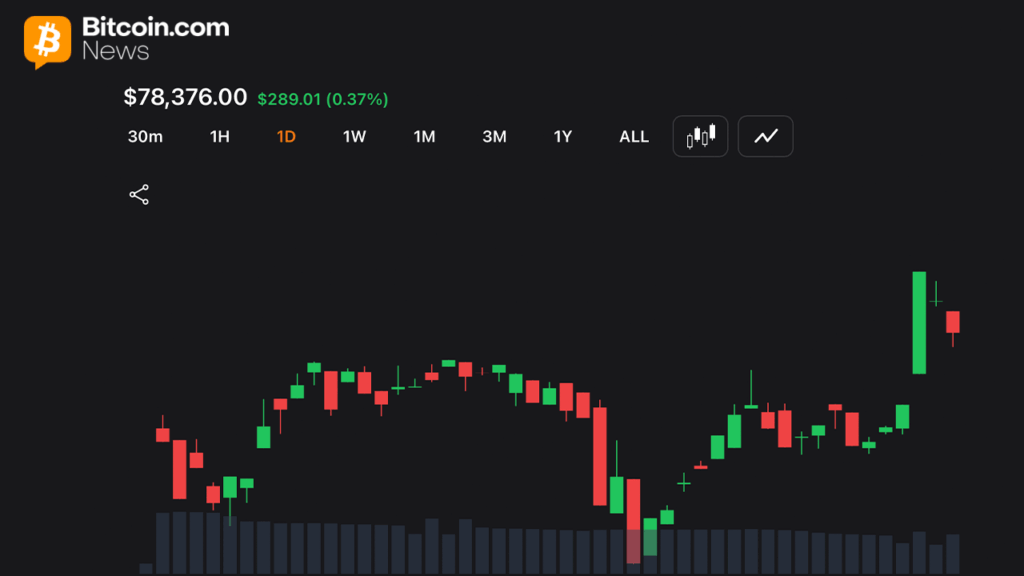

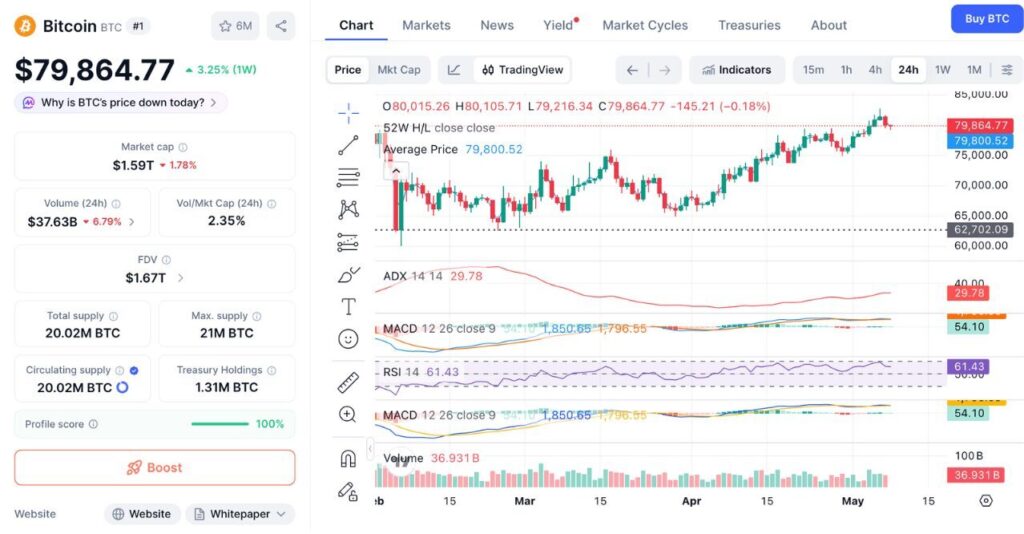

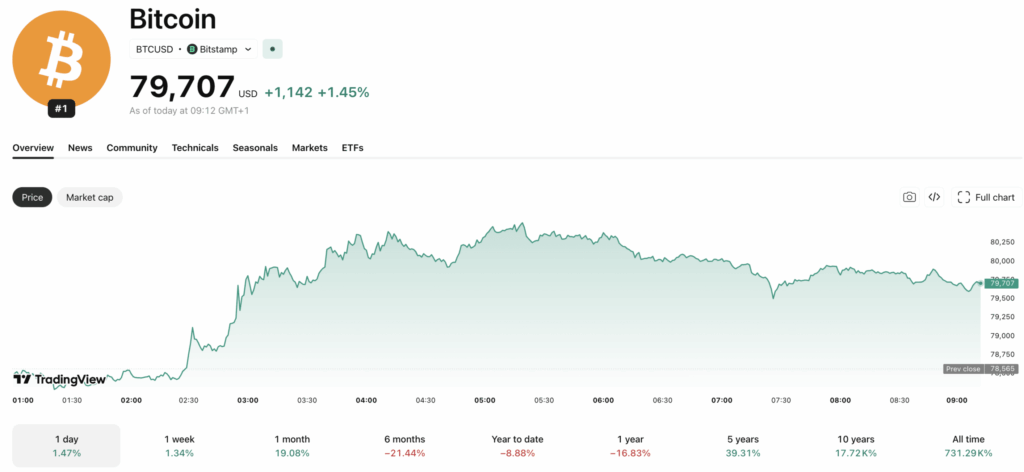

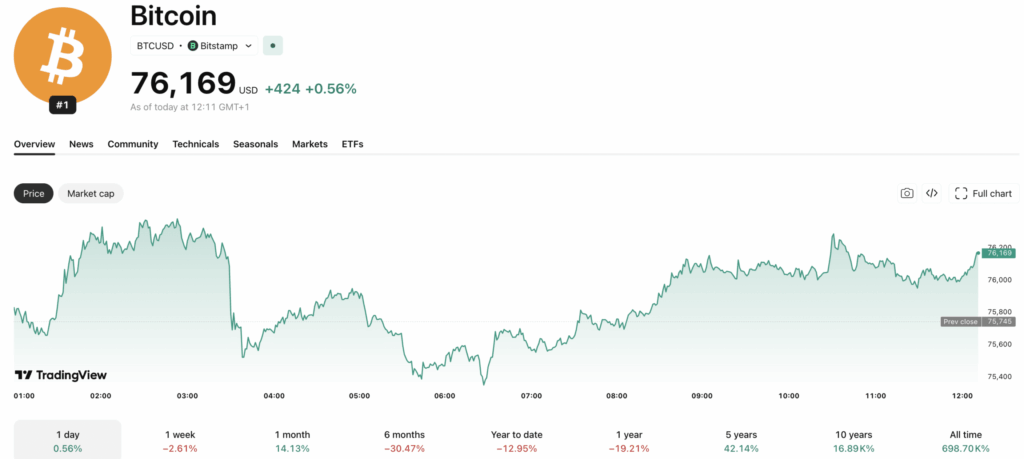

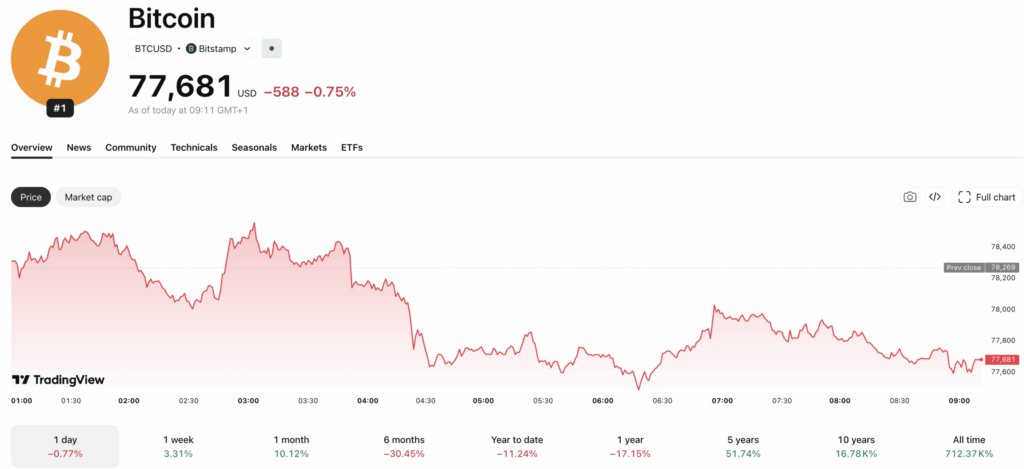

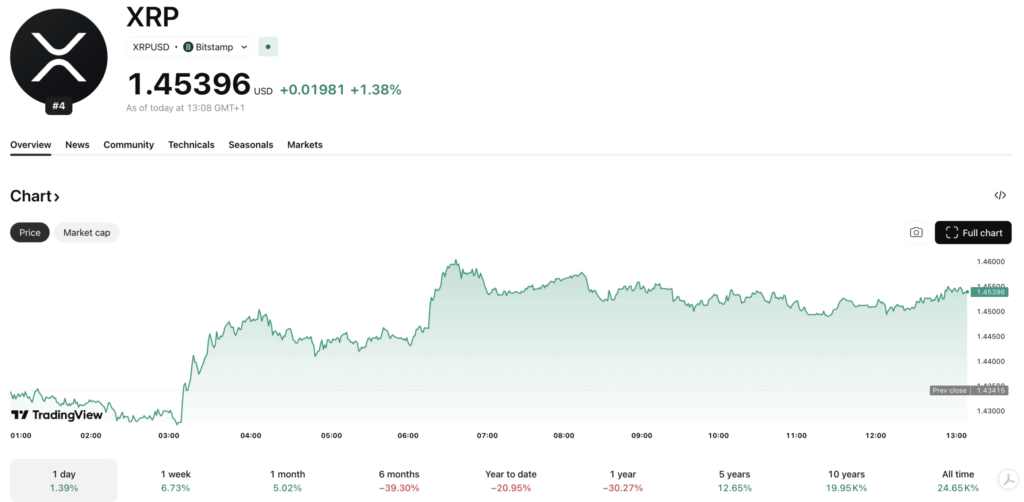

Bitcoin’s display of might continued this week, nearly touching $83,000 before finding resistance and settling in at the psychological $80,000 mark. Ethereum and solana followed suit with modest moves up, while select altcoins, particularly zcash (ZEC), drew some long-awaited attention to themselves.

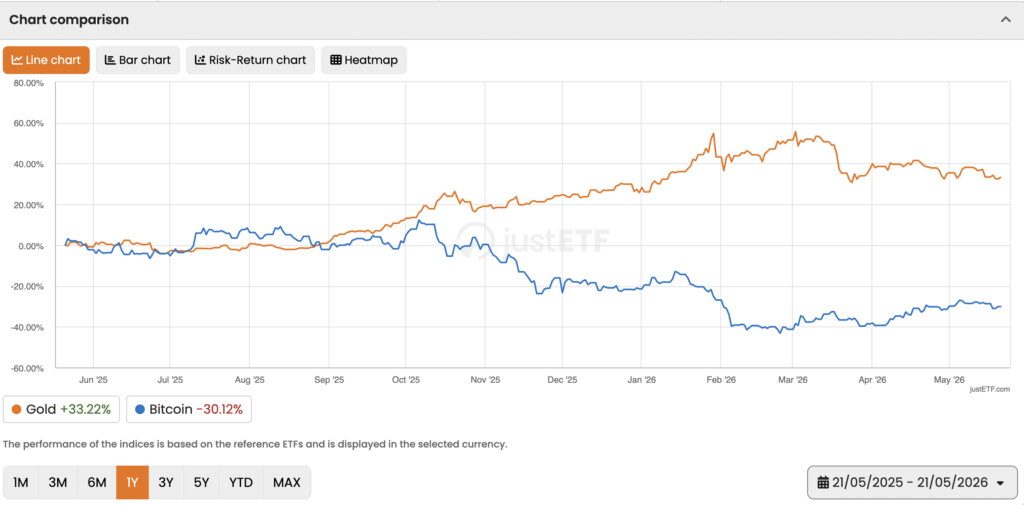

The stock market resumed its cartoonishly parabolic ascent, with the S&P 500 hitting new all-time highs on Tuesday, Wednesday, and Thursday. The Nasdaq and Russell did the same, while the Dow also inched toward another all-time high. Precious metals resumed their rebound, with gold and silver both finishing off the week in the green. Copper also had its highest weekly close near the $6.30 mark.

Crypto markets aren’t exactly having a broad-based rally. It’s more like a sorting machine, with capital and belief rising again but in narrower, sector-specific flows.

Stablecoins, as one of the strongest use cases for digital assets so far, are becoming so large and so prominent that they are arguably not “ crypto” anymore, but simply just a new part of the global financial system itself. Basically, the more useful stablecoins become, the less exotic they look. They stop feeling like tokens and start feeling like rails.

A16z argued that the term “stablecoins” will fade away for that very reason.

Other news supported that thesis. Coinbase launched USDC pairs for gold and silver perps. Kraken reportedly bought stablecoin infrastructure firm Reap for $600m. Polygon Wallet rolled out a private stablecoin sending feature. And Haseeb Qureshi made the more philosophical case that even though the major stablecoins are freezable, they remain cypherpunk enough that Hal Finney would not have been disappointed.

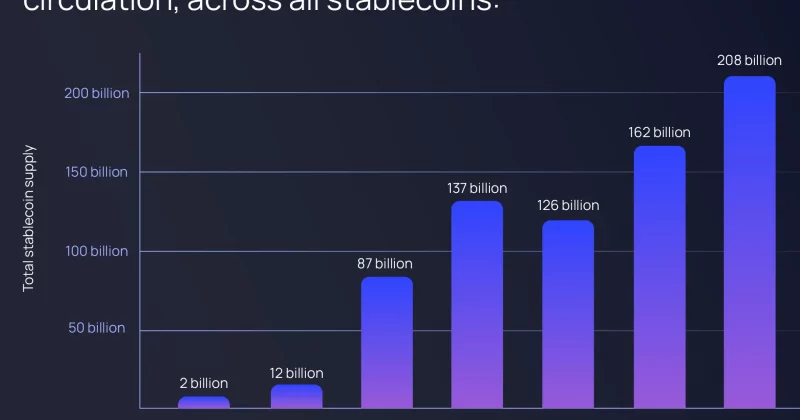

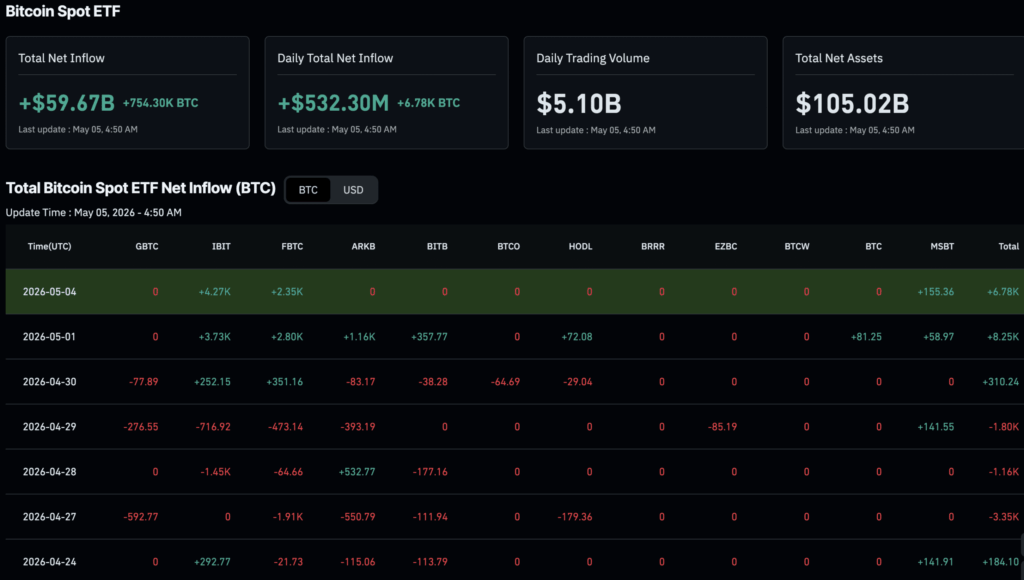

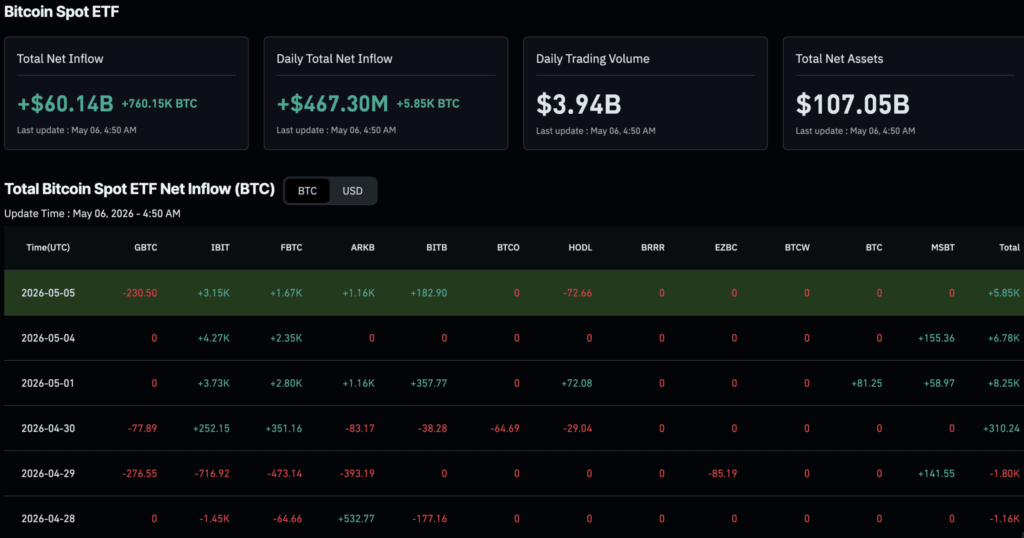

Chainalysis is now expecting stablecoin volume to reach $735 trillion by 2035. And Tether, in one of the more surreal signs of the age, now holds $20 billion in gold, effectively competing with central banks in the hard-asset accumulation game. Currently, stablecoins have a $321 billion market cap.

This is where crypto’s center of gravity may be moving. Less toward speculative abstraction, and more toward monetary plumbing and assets that sit closer to the real economy.

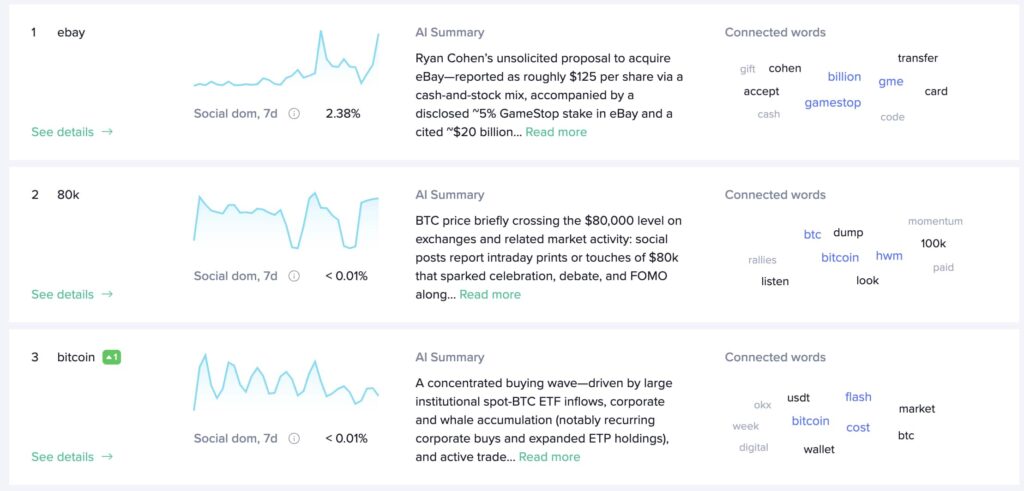

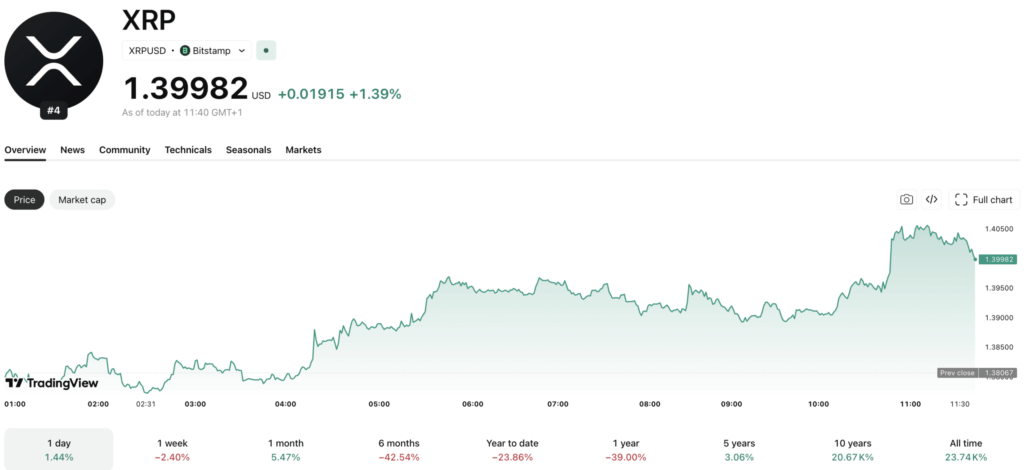

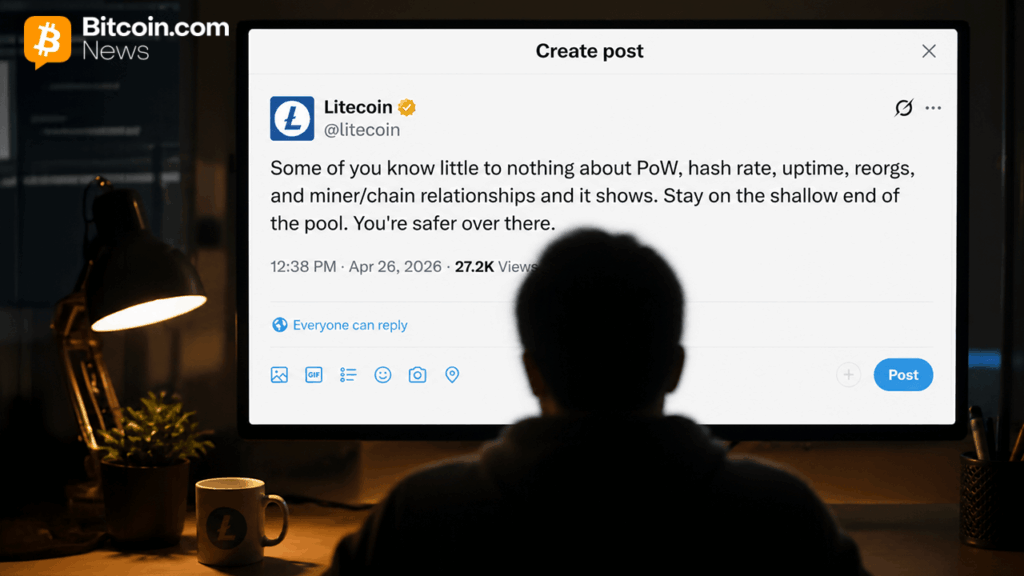

With the rise of freezable stablecoins taking hold of the crypto zeitgeist, the privacy narrative is subsequently taking off again. Zcash (ZEC) is up over 72% in the last 30 days and 1,300% in the last year. Monero’s price chart looks nearly as promising. Multicoin Capital managing partner Tushar Jain said the firm has been building a ZEC position since February, arguing that “Zcash is a return to the cypherpunk ideals crypto was founded on.” Responding to a story about the Central Bank of Brazil banning stablecoin and crypto settlement in cross-border payments, Barry Silbert, ZEC bull and Digital Currency Group (DCG) CEO said “ Difficult to ban what you can’t see. Zcash is freedom money.” Mert Mumtaz agrees.

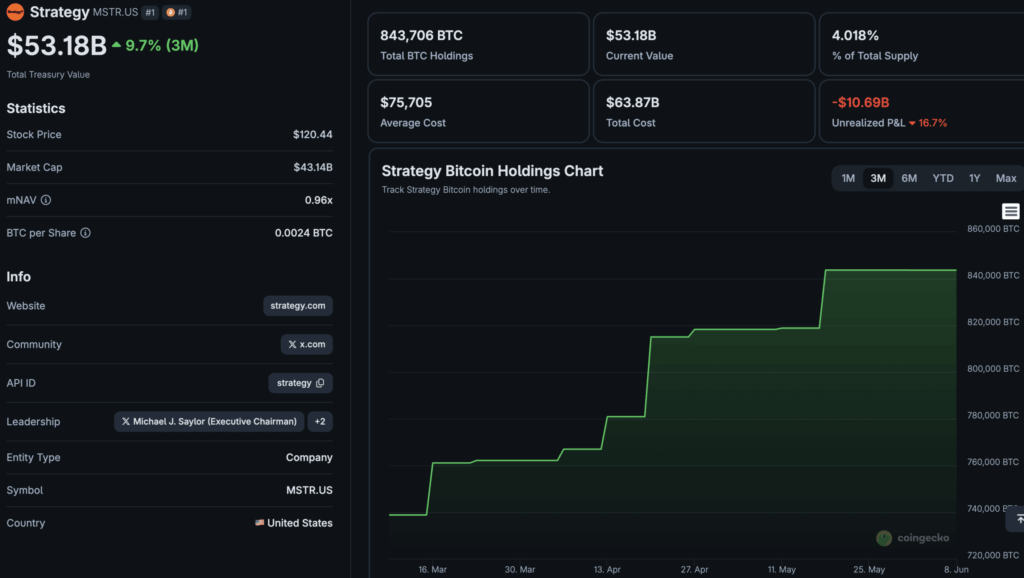

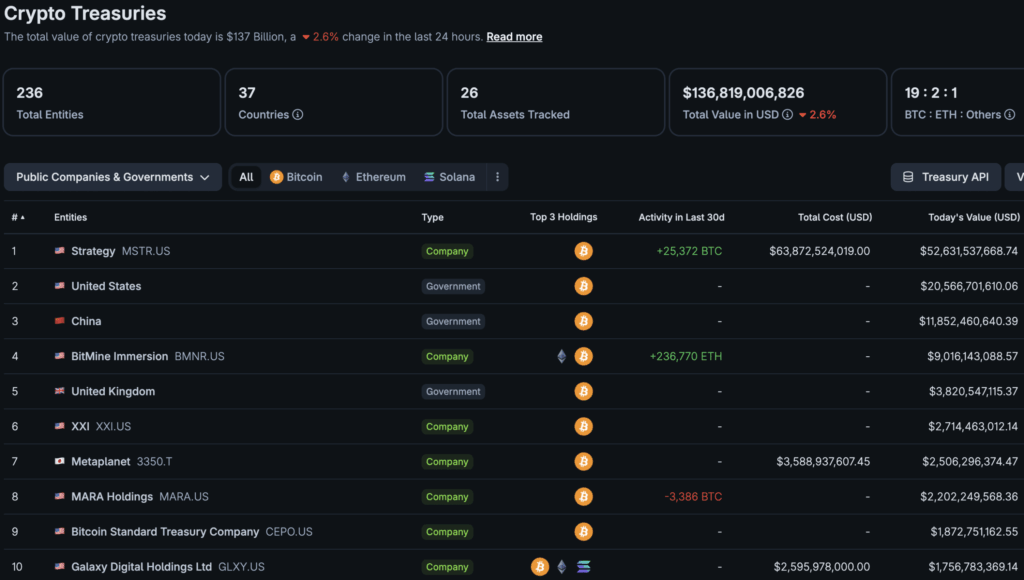

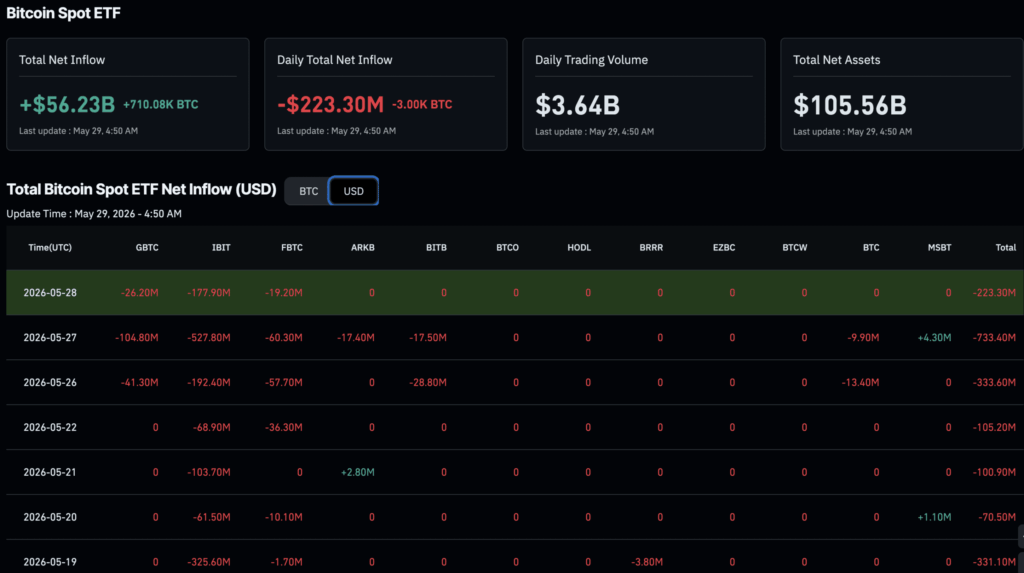

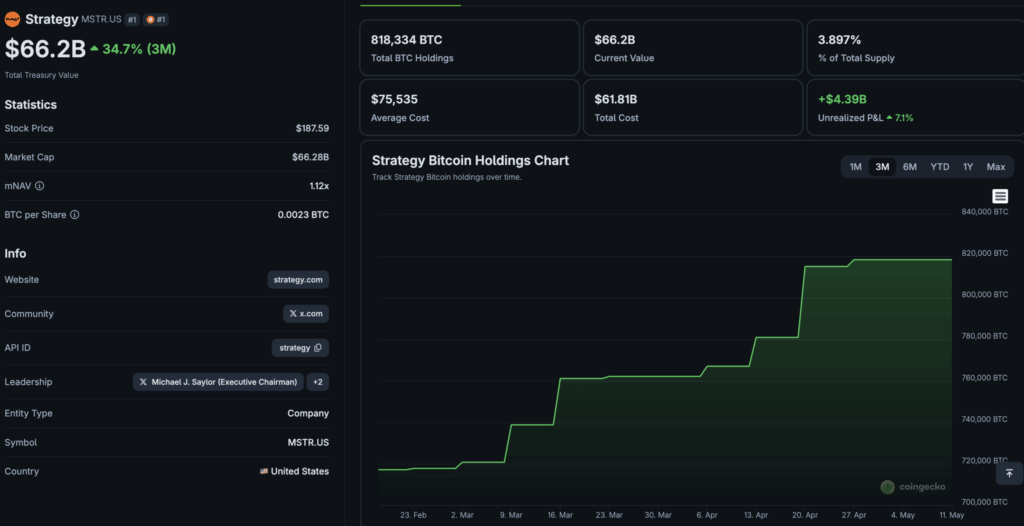

Bitcoin is strong, but the bid is changing. Jamie Coutts argued that the primary marginal bid is not ETFs anymore, but corporate treasuries. If that’s right, it probably matters a lot. ETF flows helped legitimize bitcoin, but corporate treasury demand would represent something more reflexive and more strategic: operating companies choosing bitcoin as balance sheet exposure rather than investors choosing it as portfolio exposure.

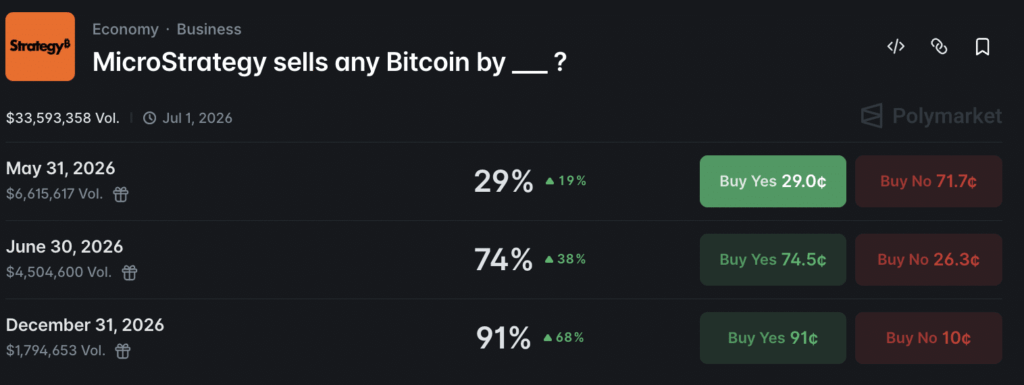

DonAlt noted that watching bitcoin pump anyway, even after Michael Saylor hinted he might sell, was something bulls love to see. A weaker asset would have wobbled on that kind of headline.

It is also happening against a backdrop where Buffett is sitting on record cash, Luke Gromen is hinting crash, and Tom Lee’s S&P target has now been hit, with the next leg of the call being a 10–15% drawdown. In other words, there is plenty of ambient macro discomfort around.

Apparently, bitcoin might not need the perfect macro backdrop these days.

Ethereum is being valued like infrastructure, not ideology. An interesting valuation frame this week came from Raoul Pal, who said the right way to think about Ethereum is to invert the question: if you turned it off, stablecoins, DeFi, L2s, and NFTs would mostly go to zero, and that total loss is the value of Ethereum.

Lookonchain says Tom Lee has now staked almost all of his ETH and should be making roughly $330 million a year in rewards at current prices. Meanwhile, Lookonchain also reports that Vitalik and the EF have sold over $100m in ETH in the last three months. Solana co-founder Anatoly Yakovenko said Ethereum L2s are not quantum safe and to “abandon all hope.”

That split is classic Ethereum. Enormous embedded economic value, meaningful infrastructure dominance, but endless opportunities for the timeline to become psychologically uninvestable.

Crypto is no longer one market, but a series of financial technologies that happen to be blockchain-based. The clearest articulation of that reality came from Cred, who said crypto’s current state is “a bit shit” and that broad-brush alt season belongs to the past. This week backed him up.

Someone tracked every Binance listing in 2025 and found that 92% are down, mostly by a lot. Pentoshi argued that crypto’s lacklustre performance is likely because AI is simply attracting all the investor attention. Coinbase is cutting 14% of staff, explicitly citing AI and a down market. Speaking of Coinbase, the US’ largest crypto exchange was down for over 6 hours on Friday morning because of an AWS outage.

The next crypto arms race may be tradfi pricing. A big theme this week was traditional finance entering crypto with the age-old strategy of undercutting everyone on price.

Bloomberg’s ETF expert Eric Balchunas highlighted that Morgan Stanley is rolling out crypto trading via ETrade with fees below Schwab, which had already undercut Coinbase. Consumer wins, obviously. But it is also a reminder that once crypto gets big enough to matter, the incumbents bring their usual weapons. “Shots fired,” said Balchunas.

That creates pressure up and down the stack. It pressures exchange fees, it pressures narrative premiums, and it pressures the idea that crypto-native firms automatically deserve higher take rates just because they were early.

The KelpDAO and LayerZero saga kept bleeding into new corners of the market this week.

Bartek Kiepuszewski’s blunt takeaway was to avoid multisig bridges altogether and stick to canonical assets and intent protocols. That is probably where the industry is heading anyway: less trust in complex bridge setups, more preference for the simplest credible path.

At the same time, lawyers for DPRK victims are now reportedly trying to get the ETH that Arbitrum managed to freeze from the hack, which suggests that once a chain or ecosystem proves it can freeze funds under pressure, the legal and political demands to do so will only grow.

Crypto has long liked to imagine a clean distinction between code and law. But once funds are freezable, that distinction gets messy.

Outside the core BTC-ETH- stablecoin axis, the week also showed how quickly adjacent market structures are maturing.

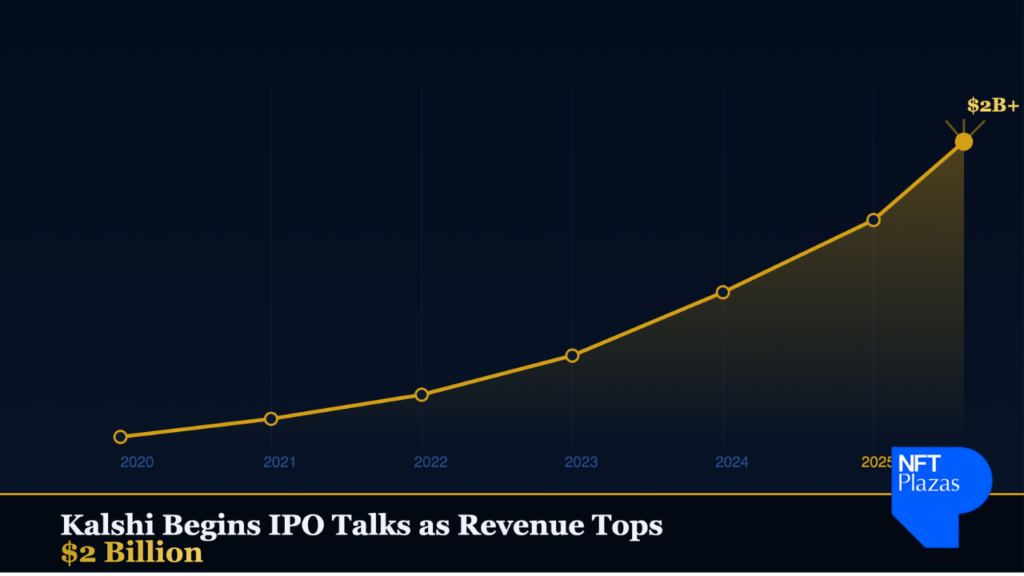

Kalshi is now valued at $22 billion, which says a lot about the market’s appetite for event trading as a durable financial category. Bullish is buying transfer agent Equiniti in a $4.2 billion deal as part of the push toward tokenized stocks. Erik Voorhees is out there answering questions on DIEM, Venice, and VVV, which is another sign that the market is still actively probing for the next model of financial internet infrastructure.

Those stories are part of the same shift: part of crypto is becoming largely about the gradual tokenization of every market surface people care to trade.

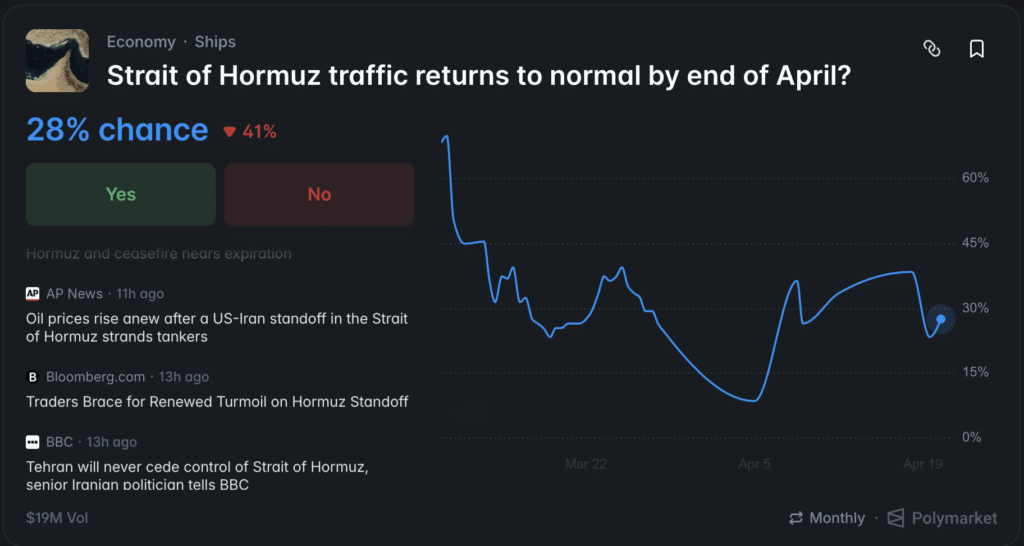

Of course, none of this is happening in a calm world. Oil is trading like some kind of cabal-run altcoin, with ridiculous volatility and flip-flopping headlines. Brent Donnelly pointed out that crude’s chart looks identical to German 2-year yields. There’s also an active debate over whether Hormuz’s closure is hurting the U.S. or actually benefiting it since U.S. oil exports are at record highs. An Iranian drone attack set a UAE petroleum complex on fire. Hantavirus is suddenly injecting lockdown-flavored fear back into the timeline.

This is often the type of backdrop where markets start behaving like rumor-sensitive nervous systems. That helps explain why crypto attention feels so fragmented. When the outside world gets more unstable, the market becomes both more opportunistic and more defensive.

There is still enthusiasm for a possible LINK mega run. Algod thinks TAO is going straight past all-time highs and says max pain is higher now that everyone has pivoted to stocks. There is an interesting theory going around about compute as a measurable commodity without a proper forward curve, which feels like the sort of idea that could eventually matter a lot if AI infrastructure starts trading more like energy infrastructure.

And in the background, Samourai dev Keonne Rodriguez is asking for donations, a reminder that even as institutional crypto matures, the people who built the older cypherpunk layer are still fighting a very different battle.

-Alex Richardson