Why the Agentic Economy Needs its Native Settlement Layer, and a Fundamental Rethink of AI Payments

Then, somewhere around 2024, I started noticing something. When a user delegates a research task to an AI agent, they don’t browse. They wait for a result. The page view, the scroll, the click, the entire surface area that advertising depends on, the model that every major internet platform like Google, Meta was built on—disappears. And I realized: if agents are going to act in the world, they need to be able to pay in the world.

If AI agents were going to act in the world, book, procure, settle, transact, how would money move?

That was the bet I made when I left Google to start AEON. Not that AI was going to be big, everyone knew that. The bet was that settlement would become the critical bottleneck in the agentic economy, and that no existing system was built to handle it.

The Unit of Value is Changing

What I was seeing was more specific: the unit of economic activity was changing. The internet economy had been organized around human behavior around clicks, sessions, and dwell time. AI agents don’t produce those signals. They produce API calls. Task completions. Automated decisions made at machine speed. The economic unit is shifting from the click to the API calls. And that shift demands infrastructure that was never built for the attention economy.

Traditional payment systems were designed for humans. KYC anchors every transaction to a human identity. Transaction volumes are calibrated to human frequencies. Fee structures that make sense for a $50 purchase become economically absurd for a $0.001 API call. The more I looked at it, the more it seemed like trying to run modern software on punch-card infrastructure.

Why Traditional Rails Hit a Ceiling

The payments industry has noticed. Visa, Mastercard, Stripe, Google, all of them have announced AI payment initiatives in the past eighteen months.

The recent Verifiable Intent framework from Google and Mastercard is a genuinely important move: by using cryptographic proofs to link identity, intent, and authorization, it begins to solve the trust problem in agentic commerce. A merchant can verify that a transaction was actually authorized by a human, not a rogue script.

But intent is only half the problem. The other half is settlement, and here, traditional rails reveal structural limits that more engineering cannot solve.

Three mismatches stand out. First, identity: KYC was designed for humans. It anchors every transaction to a passport, a bank account, a card. AI agents are code. They cannot hold passports. Stripe’s workaround, issuing virtual cards to agents, sounds elegant until you scale it: ten thousand agents generating ten thousand cards destroys the risk controls that traditional finance depends on.

Second, autonomy: most current solutions still require a human to confirm each transaction. OpenAI’s integration with Stripe is a real achievement, but the agent browses while the human pays. Remove the human from the loop and fiat infrastructure has no mechanism to verify the initiating party. That’s not agentic commerce, it’s a more convenient checkout.

Third, scale: a human making fifteen transactions a day is considered high-frequency. An AI agent handling a complex task may trigger thousands of micropayments per minute—each API call, each data query, each compute lease. A $0.30 processing fee on a $0.001 transaction is not friction. It’s economic impossibility.

These are not gaps that more capital on existing rails will close. They are architectural mismatches.

Rethink of AI Payments in the Agentic Economy

Every new payment protocol being built today, x402, AP2, ACP solves a version of “how does an agent pay.” What they share is an assumption: that there is a merchant on the other side ready to receive the payment. In practice, that merchant universe barely exists.

x402, Coinbase’s protocol for embedding payments directly in HTTP requests, is technically elegant. An agent makes an API call; the payment rides alongside it. No account setup, no human confirmation. But the receiving merchant must accept stablecoins, and today, most don’t.

In other words, the deeper constraint is settlement—how those transactions between agents complete, resolve, and connect to real-world value flows.

This is where AEON fits. We are building the settlement layer that connects these agentic protocols to the real economy. At the protocol layer, AEON integrates with emerging agentic standards including x402, ERC-8004, Google AP2, and MCP, ensuring interoperability across ecosystems and enabling seamless agent-to-agent coordination.

At the execution layer, AEON introduces a fully programmable settlement runtime, where agents can compose transaction logic in real time, including conditional payments, streaming micropayments, cross-agent escrow, and programmable compliance without human intervention.

At the infrastructure layer, AEON operates a unified node network bridging on-chain and real-world environments, allowing agent-initiated transactions to settle continuously across both digital and physical economies. Our merchant network covers more than 50 million businesses across the globe, integrated directly into national payment infrastructure like Brazil’s PIX, the Philippines’ QR Ph, and Nigeria’s NIBSS. An AI agent initiates a crypto payment; the merchant receives local currency in real time without hardware upgrades and migration.

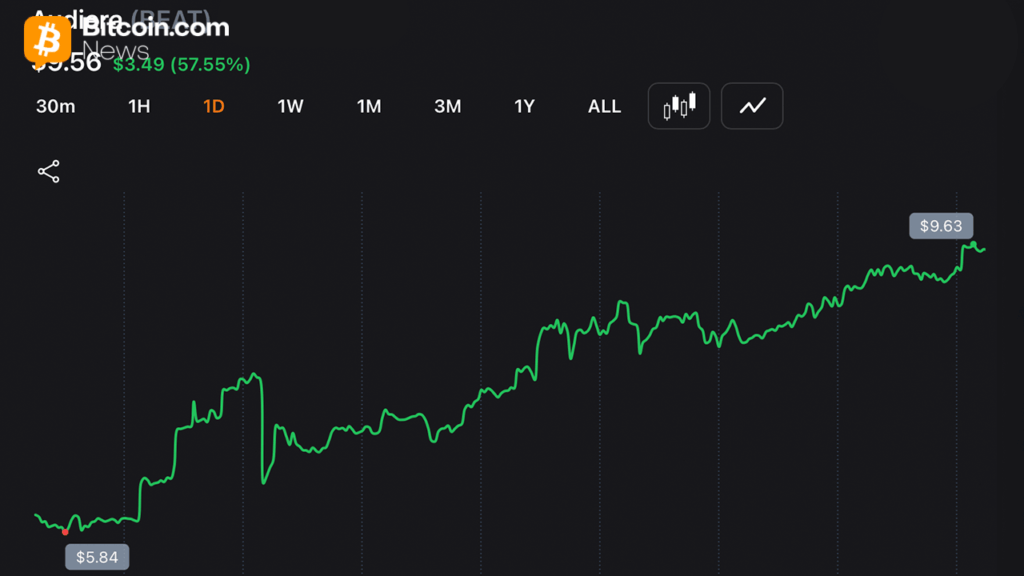

We became an official x402 ecosystem partner, launched facilitator infrastructure on BNB Chain, and integrated ERC-8004 for on-chain agent identity, a verifiable machine ID that doesn’t require a passport. Today, AEON serves over 2 million users and processes more than 30 million transactions monthly across nearly 20 emerging markets, operating at scale as an early settlement backbone for agentic finance. And we just secured investment led by the top institutions including YZi Labs, IDG Capital, HashKey Capital, Stanford Blockchain Builders Fund, and more.

What Comes Next

The protocol competition between x402, AP2, and ACP is resolving faster than most people expect. Google’s AP2 has already integrated with x402. The winner-take-all narrative is giving way to interoperability, which means the scarce resource was never the protocol. It’s the settlement layer that serves all of them.

The settlement infrastructure doesn’t dominate crypto conference agendas. It’s not a compelling narrative. There are no governance tokens, no novel consensus mechanisms, no viral mechanics. It’s regulatory relationships, local banking integrations, and currency conversion infrastructure. Deeply unglamorous.

But TCP/IP didn’t win awards. SWIFT is not a household name. The infrastructure layers that actually move value in the world are almost always invisible, almost always underestimated, and almost always more durable than the applications built on top of them.

Two waves are coming.

The first is autonomous agentic commerce: agents that don’t just recommend but execute, restocking, renewing, procuring, without a confirmation click at each step. The second is Agent-to-Agent (A2A) settlement at scale: every API call, every data query, every compute lease settled in real time between systems that never involve a human at all.

I left a stable engineering role at one of the most valuable companies in the world because I believed this infrastructure needed to be built, and that the window to build it was narrow. The giants are now confirming the thesis. But confirming a thesis and executing on the hard, unsexy problem of settlement infrastructure are different things.

The attention economy needed ad servers, tracking pixels, and bidding systems. The agentic economy needs something else. We are building it.

_________________________________________________________________________

Bitcoin.com accepts no responsibility or liability, and shall not be liable, whether directly or indirectly, for any loss, damage, claim, cost, or expense of any kind, whether actual, alleged, or consequential, arising out of or in connection with the use of, or reliance upon, any content, goods, or services referenced in this article. Any reliance placed on such information is strictly at the reader’s own risk.