The first privacy coin ETF: inside Grayscale’s Zcash filing

On May 12, 2026, Grayscale filed a Form S-3 with the SEC to convert its existing Zcash Trust into a spot exchange-traded fund trading on NYSE Arca under the ticker ZCSH.

Summary

- Grayscale filed a Form S-3 to convert its Zcash Trust into a spot ETF on NYSE Arca.

- The Zcash Trust held 391,103.89 ZEC worth about $99.4 million as of March 31, 2026.

- The SEC’s January 2026 probe closure removed a major securities-law overhang from Zcash.

- ZCSH would hold ZEC in transparent Coinbase custody, not shielded addresses.

If approved, ZCSH would be the first U.S. spot ETF for a privacy coin. The filing follows the SEC closing its long-running probe of the Zcash Foundation in January 2026 with no enforcement action, removing the regulatory overhang that had kept privacy assets out of regulated investment vehicles for years.

The Trust currently holds 391,103.89 ZEC valued at roughly $99.4 million. Coinbase Custody serves as custodian, BNY Mellon as administrator, and the fund tracks the CoinDesk Zcash Price Index. Projected inflows if approved range from $500 million to $2 billion against a roughly $6 billion ZEC market cap.

This is what the filing actually does, what the SEC’s January 2026 decision changed, and what a regulated ETF means for an asset whose value proposition rests on features the ETF itself would never use.

What Grayscale actually filed

The mechanics of the filing matter because they determine what regulatory pathway the product takes and how quickly it could reach the market.

Grayscale filed Form S-3 on May 12, 2026, which is the registration statement used by reporting companies to register securities offerings. The Form S-3 is the regulatory path for converting the existing closed-end Grayscale Zcash Trust, which has traded over the counter under the ticker ZCSH since 2017, into a spot exchange-traded fund that would list on NYSE Arca.

The same conversion mechanism was used to transform the Grayscale Bitcoin Trust into the GBTC spot ETF in January 2024 and the Grayscale Ethereum Trust into ETHE in May 2024.

The product would be physically backed, meaning the fund holds actual ZEC tokens rather than derivatives or futures contracts. Coinbase Custody serves as the custodian responsible for securing the underlying ZEC. Coinbase Inc. serves as the prime broker handling trading operations. Bank of New York Mellon serves as administrator, providing transfer agency and fund administration services. The fund tracks the CoinDesk Zcash Price Index, which aggregates ZEC pricing across major regulated exchanges to produce a single reference price.

The Zcash Trust in its current form holds 391,103.89 ZEC as of March 31, 2026, with a fair value of approximately $99.4 million. This is down from $200.4 million at the end of 2025, reflecting the price action in ZEC during early 2026 rather than any change in token holdings. The fund’s holdings represent roughly 2.3 percent of ZEC’s circulating supply.

Two characteristics of the filing are worth noting because they distinguish it from the Bitcoin and Ethereum conversions. The Trust is materially smaller than the Bitcoin and Ethereum trusts were at their respective conversions. GBTC held over $28 billion in assets when it converted. ETHE held over $9 billion. ZCSH at $99.4 million is roughly a thousandth of GBTC’s launch scale. The smaller starting size means initial trading volumes will be lower, and the structural effect on the ZEC market will be smaller in absolute terms even if it is meaningful in relative terms.

The conversion timeline under current SEC rules is also faster than it was for earlier conversions. The standard 240-day review timeline for spot crypto ETFs has been compressed to roughly 75 days under the generic listing standards the SEC adopted in late 2025. This means a Q3 2026 approval is realistic if the filing process moves forward without unusual delays.

The Bitcoin and Ethereum conversions took substantially longer in part because they were the first of their categories. The Zcash conversion benefits from the regulatory templates those earlier conversions established.

The combined effect is ZCSH, if approved, would launch as a relatively small product on a faster regulatory timeline than its predecessors. The structural significance is not the launch scale. It is the precedent the approval would set for privacy coins as a regulated investment category.

What the SEC’s January 2026 decision actually changed

The regulatory shift that made the Grayscale filing possible deserves more careful unpacking than most coverage provides.

The Zcash Foundation received a subpoena from the SEC in August 2023 as part of an inquiry into certain crypto asset offerings. The subpoena was part of the broader enforcement-led approach the SEC took toward crypto under former Chair Gary Gensler, which produced enforcement actions against major exchanges, token issuers, and DeFi protocols throughout 2023 and 2024.

The Zcash subpoena specifically created uncertainty about whether the SEC would eventually treat ZEC as an unregistered security or take enforcement action against the Foundation, Electric Coin Company, or other entities involved in Zcash development.

This regulatory overhang had practical consequences. Major U.S. exchanges were cautious about listing or maintaining ZEC support. Institutional investors generally avoided privacy coins because of the perceived enforcement risk. ETF filings for privacy coins were essentially impossible because the underlying asset’s regulatory status was unclear. The subpoena did not produce an actual enforcement action, but the open inquiry kept ZEC in a regulatory gray zone for over two years.

The SEC closed the Zcash Foundation probe in January 2026 with no enforcement action. The decision was not a formal endorsement of ZEC or privacy coins generally. It was a determination that the SEC would not pursue enforcement based on the specific facts of the Zcash inquiry. But the practical effect was substantial: the major regulatory overhang that had kept ZEC out of regulated investment vehicles was removed.

The timing of the SEC decision matters in the broader context of the regulatory environment under the new administration. The SEC under Chair Paul Atkins has taken a substantially different approach to crypto than the prior administration. The agency has dropped or settled multiple enforcement actions, approved spot ETFs for assets that had previously been blocked, including XRP, DOGE, and SOL, and adopted the generic listing standards that compress crypto ETF approval timelines.

The Zcash probe closure fits this broader pattern of the SEC stepping back from an enforcement-first approach and toward a more permissive framework for regulated crypto products.

The closure does not mean privacy coins are now uncontroversial from a regulatory perspective. The Treasury Department, FinCEN, and OFAC keep treating privacy-preserving technologies with caution from an anti-money-laundering perspective. The Tornado Cash sanctions case is still working through the courts. State-level regulations on privacy coins stay inconsistent across jurisdictions. The SEC’s January 2026 decision addresses securities law specifically, not the broader regulatory landscape for privacy assets.

But for the specific purpose of launching a U.S. spot ETF, the January 2026 decision was the key blocker that needed to be removed. With securities-law uncertainty addressed, Grayscale can pursue the standard ETF conversion pathway the Bitcoin and Ethereum trusts used. The Zcash Foundation can keep doing its work without the active enforcement threat. Other firms can begin evaluating their own privacy coin ETF filings. The ecosystem around privacy assets in regulated U.S. markets has more clarity than at any prior point.

What ZCSH would actually do for ZEC

The structural effects of an approved ZCSH ETF need to be unpacked carefully because they are different from what most coverage assumes.

The most obvious effect is institutional capital access. Investors who cannot or will not hold ZEC directly through wallets and exchanges could gain exposure through the regulated ETF wrapper. Pension funds, endowments, registered investment advisors, family offices, and other institutional categories that work under fiduciary or regulatory constraints typically cannot hold spot crypto directly. They can hold ETFs.

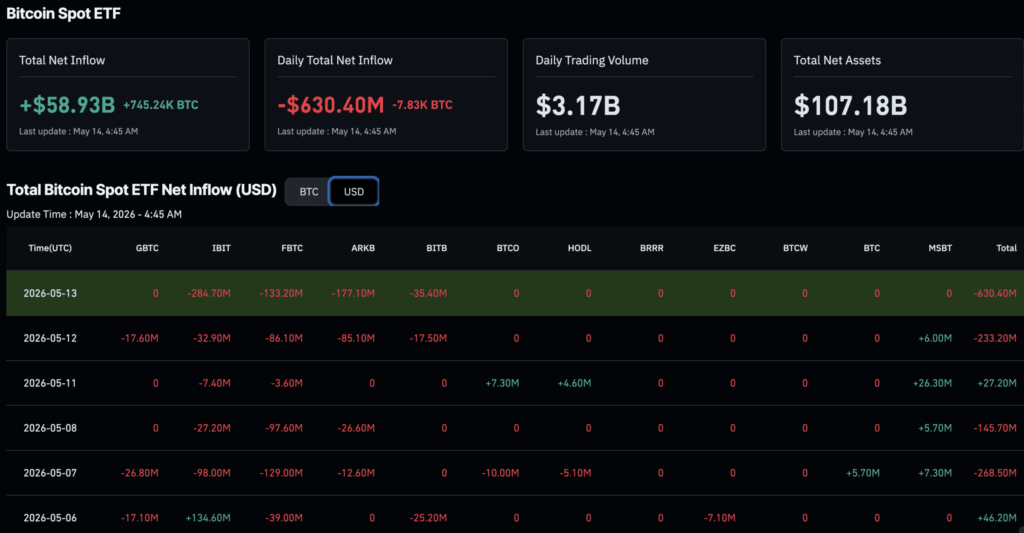

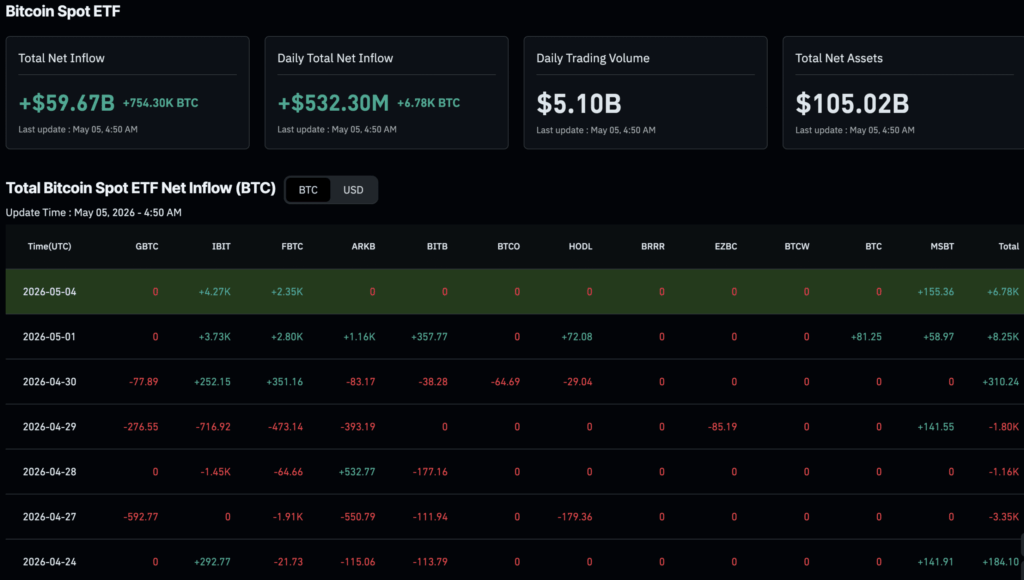

The Bitcoin ETF inflows of more than $59 billion since January 2024 show the scale of institutional capital the ETF wrapper unlocks.

For ZEC specifically, the projected inflow ranges are meaningful relative to the asset’s size. Analysts have projected $500 million to $2 billion in potential ETF inflows over the first year. Against ZEC’s current market cap of roughly $6 billion, this represents 8 to 33 percent of total market value as new institutional demand. By comparison, Bitcoin ETF inflows in the first year represented roughly 4 to 6 percent of Bitcoin’s market cap. The relative effect on ZEC could be substantially larger than the relative effect on Bitcoin, simply because ZEC’s market is smaller.

The structural effect of this new demand interacts with the supply dynamics that shielded pool growth has produced. Roughly 30 percent of ZEC’s circulating supply, or about 5 million coins, now sits in shielded addresses. That functions as a long-term holder pool that reduces effective tradable float. The effective liquid supply is closer to 11.7 million ZEC, not the 16.7 million in headline numbers. ETF inflows pulling additional ZEC out of circulation for fund holdings would further reduce the liquid float.

The Grayscale-specific dynamic adds another layer. The Zcash Trust currently trades at a persistent discount to its net asset value, which is typical of closed-end crypto trusts. Conversion to spot ETF status enables creation and redemption mechanisms that eliminate the persistent discount. Authorized participants can arbitrage any gap between the ETF’s market price and its underlying NAV, keeping the two closely aligned. The Trust’s existing ZEC holdings would, under the ETF structure, trade at fair value rather than at a discount. This NAV normalization alone could produce meaningful returns for existing Trust holders.

What ZCSH would not do is let ETF holders use Zcash’s privacy features. The fund holds ZEC in transparent custody at Coinbase. The fund’s holdings are visible on-chain. ETF investors who buy ZCSH shares are not gaining privacy protection for their own financial activity. They are gaining exposure to a token whose price is driven by other holders using the privacy features. This creates an asymmetry where the value driver, privacy adoption, and the demand driver, ETF institutional capital, are largely independent of each other.

The asymmetry is structurally important because it means the ETF can succeed commercially even if institutional holders are not interested in privacy features themselves. They are gaining exposure to a privacy asset, not using privacy infrastructure. The two are different things. The fund’s commercial viability depends on the price appreciation the underlying privacy adoption produces, which makes the ETF a structural amplifier of the shielded pool dynamics rather than a substitute for them.

Why the Coinbase custody question matters

A specific operational detail of the filing deserves attention: the custody arrangement and its effect on how the ETF can actually function.

Coinbase Custody is listed as the custodian for the Grayscale Zcash Trust ETF. This is the same custody arrangement Grayscale uses for its Bitcoin, Ethereum, and other crypto trust products. Coinbase Custody is a regulated qualified custodian under the New York State Department of Financial Services, with substantial infrastructure for holding crypto assets at institutional scale.

The complication for a Zcash-specific product is that Coinbase has limited support for Zcash’s shielded transactions. Coinbase customers can receive ZEC from shielded addresses, but Coinbase does not support sending ZEC to shielded addresses. This means Coinbase Custody holds the underlying ZEC in transparent addresses, not in shielded addresses. The fund’s holdings are visible on-chain, traceable to Coinbase Custody, and observable in real time by anyone who wants to track them.

For a normal crypto ETF, this would not matter. Bitcoin and Ethereum holdings at custodians are also transparent. The Bitcoin ETFs publicly disclose their holding addresses, and on-chain analysts can verify the holdings in real time. This transparency is generally considered a feature rather than a bug for regulated investment products.

For a privacy coin ETF specifically, the transparency creates a philosophical tension. Zcash’s core value proposition is privacy. The ETF holds ZEC in transparent custody because that custody arrangement is what regulated institutional infrastructure supports. The fund’s holdings can be observed, tracked, and analyzed in ways ZEC held in shielded addresses cannot be. The asset whose value rests on privacy features is being held by an entity that does not use those features.

The practical effects are mixed. On one hand, the transparent custody arrangement is what makes the ETF compliant with traditional financial regulation and viable for institutional adoption. Pension funds and registered investment advisors need to know exactly what their fund holds and need that information to be verifiable. Shielded custody would not meet those requirements. The transparent custody is structurally necessary for the ETF to exist as a regulated product.

On the other hand, the arrangement creates a specific dynamic where ETF growth contributes to the visible portion of ZEC supply rather than the shielded portion. If ZCSH grows to $2 billion in AUM, that represents approximately 4 million ZEC at current prices, all of which would be held in transparent addresses at Coinbase Custody. This is a meaningful percentage of ZEC’s total circulating supply being explicitly held in transparent form by a single institutional custodian.

The market dynamics produced by this arrangement are not necessarily negative for ZEC’s price. The reduction in liquid float the ETF holdings represent is real regardless of whether the ETF uses shielded or transparent custody. But the structural composition of ZEC supply would shift if the ETF reaches significant scale: a larger absolute amount in shielded addresses from continued privacy adoption, a larger absolute amount in institutional transparent custody from ETF growth, and a smaller absolute amount in retail-held transparent addresses as those holders either move to shielded addresses or sell to the ETF.

The pattern is not unprecedented. Bitcoin’s supply composition shifted similarly after spot ETF launches, with institutional custody holdings growing rapidly while exchange balances declined. The Zcash version of this pattern would just happen on a smaller scale and against a different starting composition.

What the approval timeline actually looks like

The path from filing to approval involves several specific milestones, each with its own probability and timing implications.

The Form S-3 registration statement Grayscale filed on May 12, 2026 needs to be declared effective by the SEC. Under the standard process, the registration is reviewed by the Division of Corporation Finance staff. If the staff has no further comments, the registration becomes automatically effective. If staff has comments, Grayscale responds to those comments and the registration becomes effective once the comments are resolved. For an established issuer like Grayscale with prior ETF approvals, the registration effectiveness process typically takes 30 to 60 days.

Separately, NYSE Arca needs to approve the 19b-4 rule change to list the ETF on the exchange. The 19b-4 process is the SEC’s mechanism for evaluating proposed rule changes by self-regulatory organizations, meaning the exchanges. Under the new generic listing standards for crypto ETFs, the 19b-4 process has been compressed to roughly 75 days from the standard 240 days. The 19b-4 process can extend if the SEC requests additional information or proposes amendments to the listing standards.

The combined timeline from filing to potential trading is therefore roughly 75 to 90 days under optimal conditions. This places the earliest possible launch date in late July or early August 2026. A more realistic timeline accounting for normal regulatory delays places the launch in Q3 2026, with Q4 2026 as a fallback if any unexpected complications arise.

Three specific risks could extend the timeline. The first is the SEC requesting additional disclosure about the privacy-specific characteristics of Zcash. The standard ETF disclosure documents focus on price volatility, custody risk, and operational considerations. Privacy coins introduce additional considerations, including potential regulatory action against privacy assets in foreign jurisdictions, specific operational considerations for handling shielded addresses, and tax reporting complications. The SEC may want additional disclosure about those issues.

The second risk is the SEC’s broader policy review of privacy assets. While the January 2026 decision closed the Zcash Foundation probe, the SEC has not issued formal guidance on privacy coins as an asset class. If the SEC decides to issue such guidance before approving the Grayscale filing, the approval could be delayed until the guidance is finalized. This is unlikely but not impossible.

The third risk is broader market or political developments. A major privacy-related regulatory event, such as a sanctions action against a privacy-focused service, a high-profile criminal case involving Zcash, or a Congressional hearing on privacy assets, could prompt the SEC to slow down the Grayscale approval. The current regulatory environment is friendly, but it is not static. External developments could shift the calculus.

The realistic base case is approval in Q3 2026, with the product trading by Q4 2026 at the latest. The aggressive case is approval in 60 to 75 days with launch in early Q3 2026. The pessimistic case is delays pushing approval into Q1 2027 if any of the risk factors materialize.

The CLARITY Act context

The Grayscale filing exists in a specific regulatory context shaped by the CLARITY Act, which has been working through Congress and is expected to be enacted in mid-to-late 2026.

The CLARITY Act establishes the federal framework for digital asset regulation, defining which tokens qualify as digital commodities under CFTC jurisdiction versus digital securities under SEC jurisdiction. The bill includes provisions specifically addressing how secondary market transactions in digital commodities are treated, which is directly relevant to how a Zcash ETF would operate.

Section 203 of the CLARITY Act codifies the principle that secondary market transactions in digital commodities are not securities transactions, even if the original token issuance involved an investment contract. This is the codification of the Torres framework from the SEC vs. Ripple case. For Zcash specifically, this provision would clearly establish that ZEC trading on regulated exchanges, and within the ETF wrapper, does not trigger securities-law treatment regardless of how the original token distribution was structured.

The CLARITY Act also includes the DeFi exclusion under Section 309, which protects open-source software development, validator participation, and similar activities from SEC registration requirements. This is relevant for Zcash because the Electric Coin Company and Zcash Foundation continue to be the primary developers of the Zcash protocol. Under the CLARITY Act, their development activities would have clear legal protection from securities-law treatment.

The interaction between the CLARITY Act framework and the Grayscale ETF approval matters because it provides a more durable foundation for the ETF’s regulatory treatment. The January 2026 SEC decision was an enforcement decision specific to the Zcash Foundation probe. The CLARITY Act, once enacted, provides statutory clarity that goes beyond a single enforcement decision. An approved ZCSH ETF running under the post-CLARITY framework has substantially more regulatory durability than one operating only under the prior enforcement decision.

The timing question is whether the CLARITY Act enactment precedes or follows the ZCSH approval. The current Senate Banking Committee markup occurred in May 2026. Floor votes are expected in summer 2026. House reconciliation could push final enactment to late 2026. If ZCSH approval comes first, the ETF launches under the existing enforcement-decision framework. If CLARITY enactment comes first, the ETF launches with full statutory backing. Either sequence is plausible.

For the broader privacy coin category, the CLARITY Act framework matters even more than for Zcash specifically. Other privacy assets that have not received SEC enforcement decisions, including Monero and Dash, would benefit from the statutory clarity CLARITY provides. The Zcash ETF could be the first privacy coin ETF, but it is unlikely to be the last if the regulatory framework holds and the institutional demand patterns observed with ZCSH carry over to other privacy assets.

Comparison to other privacy coins

The natural question raised by the Grayscale filing is what it means for the broader privacy coin category, particularly Monero, which has historically been the most-discussed privacy coin alongside Zcash.

The categorical differences between Zcash and Monero are structurally important for regulated investment products. Zcash is privacy-optional, meaning users can choose between transparent and shielded addresses. This flexibility lets Zcash maintain custody arrangements with regulated entities like Coinbase, even though those entities only support the transparent portion of the network. Monero is privacy-mandatory, meaning all transactions are private by default with no transparent option. This makes Monero fundamentally incompatible with traditional custodial infrastructure, because the custodian cannot show the specific assets it holds in the way regulated investment products require.

The practical consequence is that a Monero ETF is substantially more difficult to structure than a Zcash ETF. Coinbase Custody can hold ZEC in transparent addresses, show the holdings to auditors and regulators, and produce the verification documentation regulated investment products require. The same custody arrangement is structurally impossible for XMR because every Monero address is private. Any Monero custody arrangement faces the regulatory challenge of showing compliance with anti-money-laundering requirements that depend on transaction visibility.

This is why Grayscale filed a Zcash ETF specifically rather than a generic privacy coin ETF or a Monero ETF. The technical architecture of Zcash makes it compatible with regulated investment infrastructure in ways Monero is not. The privacy-optional design some Monero advocates have historically criticized as weak privacy turns out to be the feature that makes Zcash institutionally viable.

For other privacy-adjacent assets, the effects are mixed. Dash uses optional privacy features through PrivateSend mixing. Decred has shielded transactions through the Schnorr signature implementation but limited adoption of the privacy features. Newer zero-knowledge protocols on Ethereum and other smart contract platforms offer privacy at the application layer but not at the base layer. Each of these has different regulatory and custody profiles than either Zcash or Monero.

If ZCSH is approved and trades successfully, the most likely follow-on filings are for Dash and possibly Decred, where the privacy-optional architecture provides a similar regulatory pathway to Zcash. Monero ETF filings stay unlikely in the near term given the structural custody challenges.

The broader point is that the Grayscale filing represents a specific bet on Zcash’s regulatory positioning rather than a generic bet on privacy as a category. The fund’s approval would validate Zcash’s particular architectural choice, optional privacy with transparent fallback, as the model for regulated privacy investment products. This has effects on how other privacy-focused projects might position themselves over time. Projects that want institutional capital may face structural pressure to adopt similar privacy-optional architectures rather than privacy-mandatory designs.

What could go wrong

A complete analysis has to name the conditions under which the Grayscale ETF approval could fail or the ETF’s commercial viability could disappoint.

The first risk is approval denial. While the January 2026 SEC decision substantially improved the probability of approval, denial is not impossible. The SEC could decide privacy coin ETFs require additional regulatory development before approval, particularly if the Treasury Department or FinCEN raises specific concerns about anti-money-laundering compliance. A denial would not necessarily be permanent, but it would push the timeline meaningfully and signal privacy coins stay a special regulatory category.

The second risk is approval with restrictive conditions. The SEC could approve the ETF but impose specific restrictions, including limited custody arrangements, additional disclosure requirements, or geographic limitations that constrain the product’s commercial viability. Bitcoin and Ethereum ETFs run under specific conditions, and a Zcash ETF would likely face additional conditions given the privacy-specific considerations. If those conditions are too restrictive, the projected inflow ranges could be substantially lower than the $500 million to $2 billion estimates.

The third risk is institutional demand disappointment. Even with approval and no restrictive conditions, the ETF could fail to attract the projected institutional capital. The investor base for privacy coins is structurally smaller than for Bitcoin or Ethereum. Many institutional investors have explicit policies against privacy-focused assets due to anti-money-laundering compliance concerns. The actual addressable market for ZCSH may be substantially smaller than the headline market cap of ZEC suggests.

The fourth risk is regulatory reversal at the federal level. The current SEC’s permissive approach to crypto, including the January 2026 Zcash decision, is not permanent. A future change in administration or political pressure could reverse the regulatory posture. If the SEC under a future administration took a more restrictive view of privacy coins, the ZCSH ETF could face delisting or operational restrictions even after launch. This is a longer-term risk affecting the durability of the institutional adoption thesis.

The fifth risk is state-level or international regulatory pressure. Even if the federal regulatory environment stays friendly, state regulators or international jurisdictions could take restrictive positions on privacy coins. Japan and South Korea have at various times restricted exchange listings for privacy coins. State-level money transmission laws could create complications. Privacy coin restrictions in major foreign markets could limit the ETF’s commercial viability by reducing the global pool of accessible capital.

None of these risks make approval or commercial success impossible. They are the specific conditions under which the optimistic case could fail. The honest read is that the probability of ZCSH approval is high, probably in the 75 to 85 percent range based on the current regulatory environment, but the probability of the optimistic inflow projections is lower, probably 40 to 60 percent for the full $500 million to $2 billion range. The base case is approval with modest commercial success rather than approval with breakthrough institutional adoption.

What to watch

For readers tracking the ZCSH filing through to potential approval and launch, four specific milestones are worth watching over the coming months.

The first is the SEC’s response to the Form S-3 registration. Staff comments on the registration statement will become public when Grayscale responds to them. The nature of the comments will signal what specific concerns the SEC has about the product structure. Routine comments about disclosure language suggest a smooth approval path. Substantive comments about custody arrangements or privacy-specific risks suggest more complicated review.

The second is the NYSE Arca 19b-4 filing and the SEC’s response. The 19b-4 process under the generic listing standards should take roughly 75 days. The SEC’s response on the 19b-4 will signal whether the agency views privacy coin ETFs as falling within the standard listing framework or requiring special treatment.

The third is the CLARITY Act progression through Congress. If the bill is enacted before the ZCSH approval, the ETF launches with full statutory backing. If enactment comes after, the ETF launches under the existing enforcement-decision framework, which is less durable. The relative timing of the two will affect the long-term regulatory foundation of the product.

The fourth is institutional positioning around the filing. The Multicoin Capital disclosure of February 2026 ZEC accumulation is one signal. Additional disclosures from other major funds, asset managers adopting ZEC positions, or family office allocations becoming public would indicate growing institutional conviction in the ETF’s prospects. Conversely, institutional exits or public statements of skepticism would signal lower confidence in the structural thesis.

The bottom line

The Grayscale Zcash ETF filing is the most significant regulatory development for privacy coins in the asset class’s history. The approval of ZCSH would create the first U.S. spot ETF for a privacy coin, establish a regulatory template for similar future products, and provide institutional access to an asset category that has previously been structurally excluded from regulated investment vehicles.

The mechanics of the filing are straightforward. Form S-3 conversion of an existing closed-end trust into a spot ETF, listing on NYSE Arca under the ticker ZCSH, Coinbase Custody as custodian, BNY Mellon as administrator, tracking the CoinDesk Zcash Price Index. The Trust’s current $99.4 million in ZEC holdings would convert to ETF status, with creation and redemption mechanisms eliminating the persistent NAV discount that has characterized the closed-end product.

The regulatory pathway is enabled by two specific developments. The SEC’s January 2026 closure of the Zcash Foundation probe removed the major enforcement risk that had kept privacy assets out of regulated investment vehicles. The generic listing standards the SEC adopted in late 2025 compressed the ETF approval timeline from 240 days to roughly 75 days, making the launch achievable in Q3 2026. The CLARITY Act framework, once enacted, would provide additional statutory clarity that goes beyond the enforcement-decision foundation.

The structural significance for Zcash specifically is the institutional capital access the ETF would unlock. Projected inflows of $500 million to $2 billion represent 8 to 33 percent of ZEC’s current market cap as new institutional demand. Combined with the shielded pool dynamics that have already reduced effective liquid float to approximately 11.7 million ZEC, the ETF inflows would produce structural upward pressure on price the current market is not fully pricing in.

The asymmetry between the ETF and the underlying asset is the analytically interesting feature. ZCSH holders gain exposure to ZEC’s price appreciation without using Zcash’s privacy features themselves. The fund’s holdings are transparent at Coinbase Custody, not shielded. The value driver, privacy adoption that produces shielded supply growth, and the demand driver, ETF institutional capital, are largely independent. The fund succeeds commercially because of the price appreciation privacy adoption produces, even though the fund’s own investors are not using privacy features.

For the broader privacy coin category, the effects depend on whether ZCSH approval extends to other privacy assets. Zcash’s privacy-optional architecture is what makes the ETF structurally viable. Monero’s privacy-mandatory design is fundamentally incompatible with traditional custodial infrastructure, which means a Monero ETF stays unlikely regardless of regulatory environment. Privacy-optional designs like Dash and Decred could follow Zcash’s pathway. Privacy-mandatory designs cannot easily replicate the model.

The honest read of the situation is that ZCSH approval is probable, in the 75 to 85 percent range based on current regulatory conditions, while the commercial success of the product is uncertain. The $500 million to $2 billion inflow range is optimistic, with $100 million to $500 million more realistic for the first year. The broader significance for privacy coins as an asset class is genuinely meaningful. The first privacy coin ETF in the U.S. is a structural milestone whether the specific product is commercially successful or modest.

For ZEC holders, the practical implication is that the ETF approval timeline is the next major catalyst after the May 2026 rally that pushed ZEC above $600. Approval in Q3 2026 would provide structural support for the price even if the broader crypto market enters a weaker phase. Approval denial would be a meaningful negative signal that would likely produce a price correction. The probability-weighted expected value is positive, but the variance is meaningful.

For the broader market, the ZCSH filing represents the institutional crypto industry’s bet that privacy is a regulated asset category rather than a prohibited one. Grayscale is putting its regulatory relationships and product development resources behind that bet. If they are right, ZCSH is the first of multiple privacy coin ETFs that will reach the market over the next several years. If they are wrong, the filing is an experiment that establishes the limits of what regulated U.S. crypto products can include.

Either way, the filing is making explicit what was previously implicit: the question of whether privacy assets can be packaged for institutional investors is no longer theoretical. It is an operational question with a specific answer arriving in Q3 2026.

The answer will shape the structural composition of crypto markets for years.

This article is for informational purposes and does not constitute financial or investment advice. ETF approvals and regulatory timelines evolve quickly; the figures and milestones described reflect reporting available as of late May 2026. Always do your own research.