$8 Billion Bitcoin Attack Could Become Profitable Through Derivatives, Duke Professor Says

Key Takeaways

- Campbell Harvey says an $8 billion 51% attack could pair Bitcoin hashpower with shorts.

- Duke University’s model puts the cost near 0.5% of bitcoin’s value, challenging market assumptions.

- In 2026, bitcoin miners and exchanges face questions over how they would counter such an attack.

Harvey outlined the argument on Scott Melker’s “The Wolf of All Streets” podcast, describing a theoretical operation in which a well-funded group spends about $8 billion to gain majority control of Bitcoin’s computing power while building a large short position against the asset. The episode appeared on X. The proposal centers on a 51% attack, a risk embedded in Bitcoin’s design since Satoshi Nakamoto published the network’s white paper in 2008.

A Risk Known From Bitcoin’s Beginning

An entity controlling more than half of the network’s hashpower could produce blocks faster than honest miners, create the longest valid chain, and influence which transaction history nodes accept. Such an attack could enable double-spending, transaction censorship or the reorganization of recent blocks. It would not allow an attacker to create unlimited bitcoin or seize coins without valid signatures, but it could damage the network’s credibility by showing that its transaction record could be manipulated by concentrated computing power.

For years, the prevailing economic argument against the scenario has been fairly straightforward. An attacker would need to buy or control enormous quantities of specialized mining equipment, secure data center capacity, and consume vast amounts of electricity. A successful attack could then have a strong chance at destroying confidence in BTC, pushing down the value of the very asset needed to recover those costs.

Harvey said that logic made the attack difficult to justify except as an act of geopolitical sabotage. “Why would you spend billions of dollars investing in mining equipment?” he asked. “You spend all this money, and then you take over the network, but the price of bitcoin would collapse to zero.” His thesis is that derivatives markets have changed the calculation. “The difference today is the derivatives markets,” Harvey remarked on Melker’s show, pointing to liquid offshore venues where traders can establish short positions that gain value when bitcoin falls.

How the Trade and Attack Would Work Together

Under Harvey’s model, the attacker would quietly assemble mining hardware and supporting infrastructure while opening a substantial short position in bitcoin. The network attack would then be used to undermine confidence, pressure the price, and increase the value of the short.

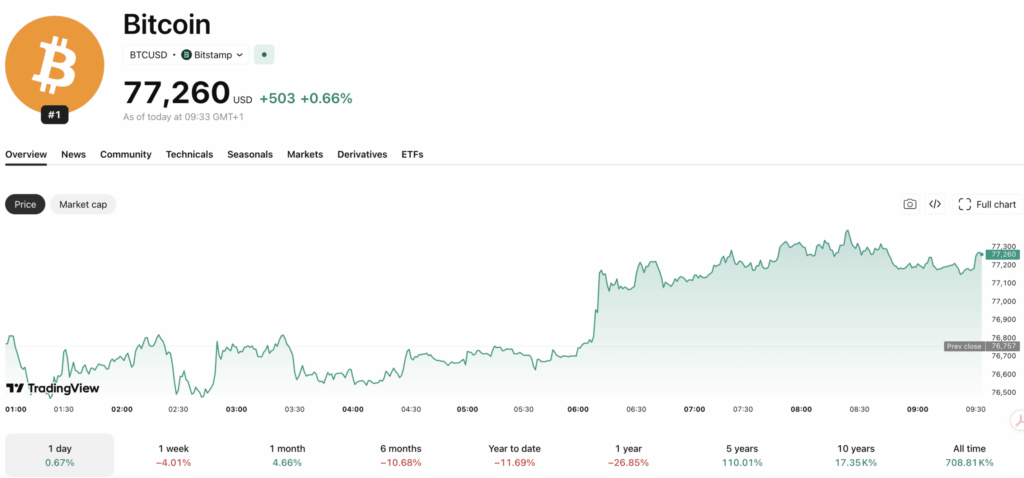

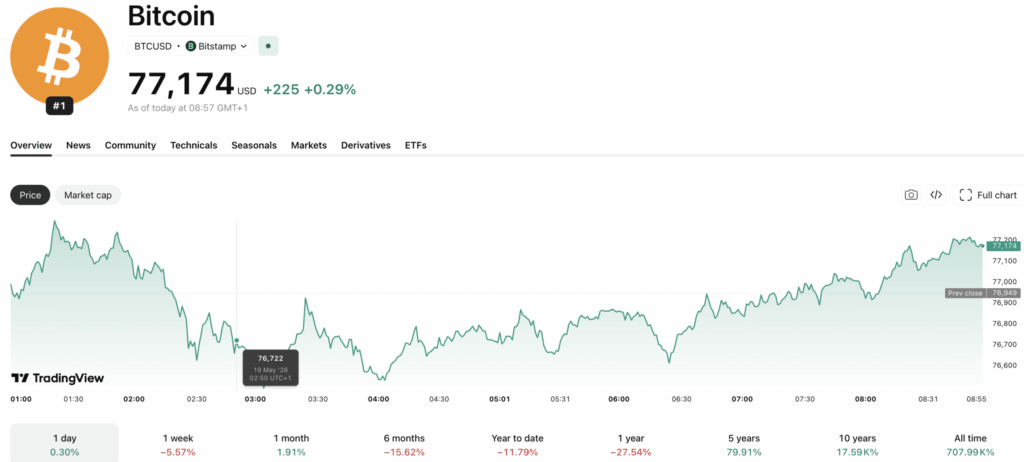

“The cost is about 50 basis points of the value of bitcoin,” Harvey told “The Wolf of All Streets” podcast host, referring to roughly 0.5% under the assumptions discussed in his work. He placed the attack cost near $8 billion in the podcast, although estimates depend on hardware prices, energy costs, network hashrate and the duration of the attempted takeover.

The attack and the financial trade are inseparable in this framework. Mining rewards would not need to repay the investment. Instead, profits from the derivatives position could offset the cost of equipment, construction and electricity. Harvey stressed that an attacker would “simultaneously during the attack take a short position in bitcoin,” making a severe price decline the intended source of repayment.

Harvey also argued that the market impact could begin before any attack. A consortium announcing plans to build a mining operation large enough to threaten the network could create fear, weaken sentiment and pressure prices even if the group never gained majority control.

Practical Barriers Remain Substantial

The scenario is theoretical, and Harvey did not claim an attack is imminent. Building enough capacity would require access to billions of dollars, large supplies of advanced mining machines, extensive power infrastructure, and coordinated execution. Those preparations could become visible through semiconductor orders, data center construction, electricity agreements, or unusual derivatives activity.

Bitcoin also has defensive options outside the narrow mechanics of the longest-chain rule. Exchanges could limit suspicious positions, miners could redirect computing power, and developers and users could coordinate software changes or reject an attacker’s chain. Any such response could be disruptive, politically contentious, and difficult to organize quickly, but it complicates the assumption that an attacker could operate without resistance.

Harvey contrasted bitcoin with gold, arguing that gold has no comparable network mechanism that could be captured to rewrite ownership history or halt transaction processing. His broader conclusion is not that BTC is certain to fail, but that investors should treat network control and derivatives incentives as a distinct tail risk when comparing BTC with traditional stores of value.

Melker Pushes Back on Specific Scenarios

Melker pushed back some after Harvey laid out the thesis. His pushback focused on execution rather than dismissing Harvey’s financial logic. He argued that an $8 billion mining buildup would be “pretty highly telegraphed,” since acquiring enough application-specific integrated circuit (ASIC) miners, data center space, and electricity to approach 51% of Bitcoin’s total hashpower would leave a visible trail.

Manufacturers, power providers, mining companies, and market participants could detect the expansion before it reached operational scale, giving miners, exchanges, developers, and users time to prepare technical or economic responses. Melker also questioned whether a successful attack would drive bitcoin close enough to zero for the short position to recover billions of dollars in costs.

He noted that other proof-of-work ( PoW) networks have survived 51% attacks and said the project would involve “the mining, the setup, the time, the electricity and a lot of other factors.” Harvey responded that his estimate accounted for equipment, infrastructure, power, wear, and higher ASIC prices caused by increased demand. Melker nevertheless concluded that the derivatives-based motive was worth examining, calling it “merely a financial motive” that could turn network sabotage into an economic calculation.

For markets, the thesis raises questions that extend beyond mining. It asks whether offshore leverage, concentrated infrastructure, and financial engineering can create incentives that Bitcoin’s original security model did not fully anticipate. If Harvey’s thesis has legs, the central issue is no longer only whether a 51% attack is technically possible, but whether modern markets could make one economically rational.