What is CASHCAT? Robinhood Chain’s memecoin

CASHCAT is a token named after a company name that was thrown away sixteen years ago. It reached a $156 million market cap, briefly outweighed every real asset on Robinhood’s blockchain, and its own website calls it fan fiction with a ticker.

Summary

- CASHCAT is a community memecoin on Robinhood Chain with a fixed supply of one billion tokens. It has no affiliation with Robinhood Markets, and its own site says so.

- The name comes from real history: before Robinhood was Robinhood, Vlad Tenev and Baiju Bhatt called their company CashCat. A New Yorker profile preserved the detail and a token resurrected it.

- It surged more than 2,100% in a week to a market cap near $156 million, at one point worth roughly twelve times every tokenized real-world asset on the chain combined.

- CEO Vlad Tenev dismissed utility-free assets on July 2, then posted six days later that the chain works great for memes too, and followed the token’s account.

- The token fell more than 33% in 24 hours after Noxa, the launchpad driving the boom, stopped accepting launches on July 11 and went dark two days later.

In 2010, two Stanford graduates building a trading company had a name for it. The name was CashCat. They discarded it, called the company Robinhood instead, and the detail survived only in a New Yorker profile and in the memory of people who read startup lore for fun. Sixteen years later, Robinhood launched a blockchain designed to settle tokenized stocks for institutions, and within days the busiest thing on it was a token named after the name they threw away. CASHCAT reached a market capitalization near $156 million, out-massed every real asset the chain was built for, and made a handful of anonymous wallets millionaires. Its website describes it as fan fiction with a ticker. That is not a criticism. It is the project’s own self-assessment, and it is more honest than most.

The basics

CASHCAT is a memecoin native to Robinhood Chain, the Ethereum layer 2 that Robinhood launched on July 1, 2026. For readers new to the network, crypto.news has also explained the chain it launched on.

Its supply is fixed at one billion tokens, with no further issuance. Its contract address is 0x020bfC650A365f8BB26819deAAbF3E21291018b4, and verifying that string against a trusted source before any transaction is the single most useful thing in this article. It does not have its own blockchain or application. It is a fungible token deployed on someone else’s chain, which is what almost every memecoin is.

It has no product, no roadmap in any meaningful sense, and no utility. The project does not pretend otherwise. Asked what the utility is, the site answers that the utility is cat.

Most importantly, and against what a large number of buyers appear to believe: it is not a Robinhood product. It is not owned, endorsed, backed, listed, or affiliated with Robinhood Markets in any way, and the token’s own website disclaims any connection to the company or to Tenev personally.

Where the name comes from

The connection is entirely historical and it is worth getting right, because the ambiguity is the asset.

Before the company became Robinhood, Tenev and co-founder Baiju Bhatt called their venture CashCat. The detail appears in a New Yorker profile of the company and had circulated among people who follow startup history for years. When Robinhood Chain launched, someone recognized that a discarded corporate name attached to a live corporate blockchain was a nearly perfect memecoin: instantly legible to anyone who knew the story, plausible to anyone who did not, and impossible for the company to claim without endorsing it.

That is the entire link. A name the founders rejected in 2010, revived as a token in 2026 by people with no relationship to them. There is no corporate partnership, no licensing arrangement, and no shared ownership. What exists is a shared piece of trivia, and the token converted that trivia into a market capitalization.

There is a small extra layer that fueled it: Tenev himself had tweeted about CashCat back in April 2021, which meant the lore was not merely documented but personally acknowledged by the CEO years before the token existed. None of that constitutes affiliation. All of it makes affiliation feel more plausible than it is.

What happened

The timeline is short and steep.

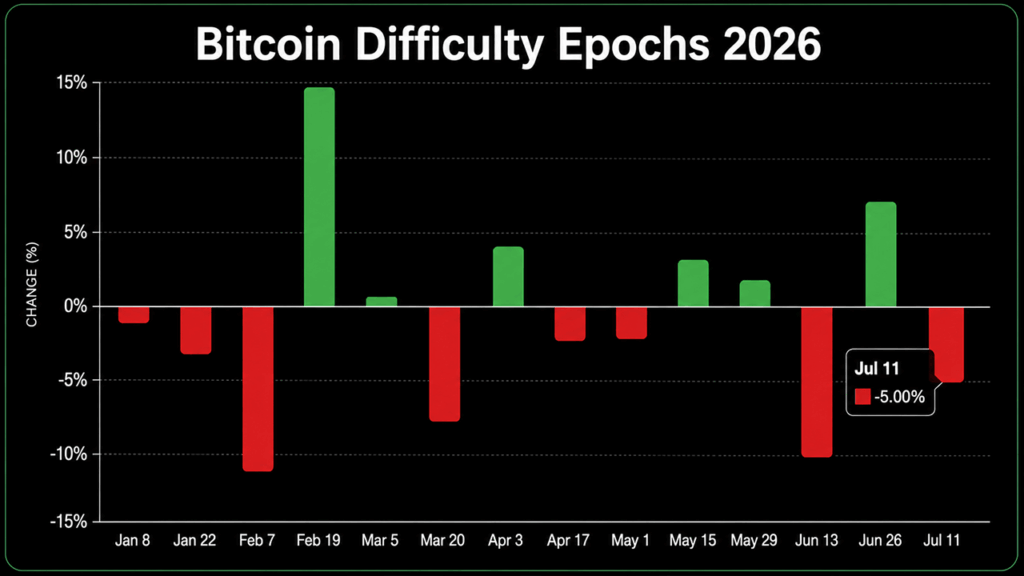

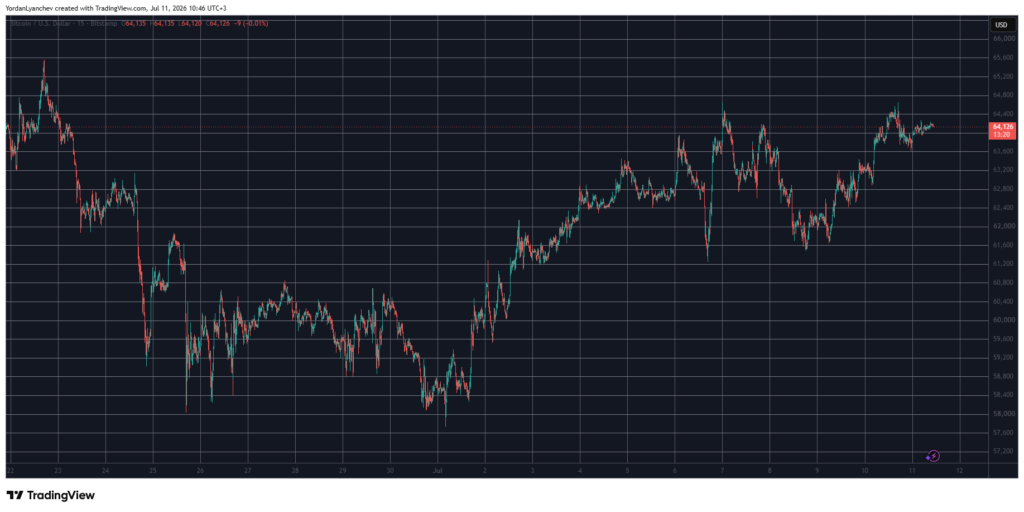

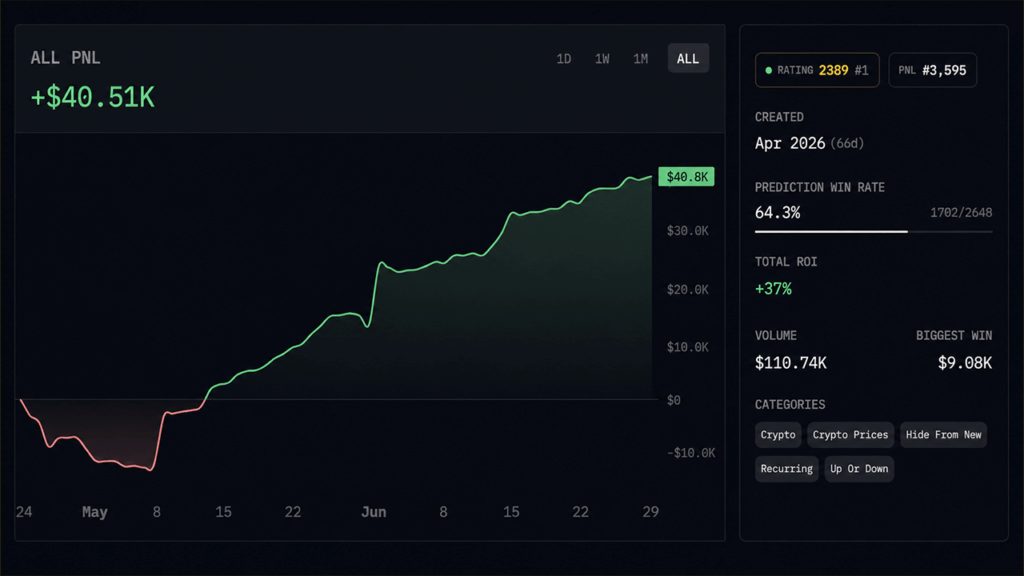

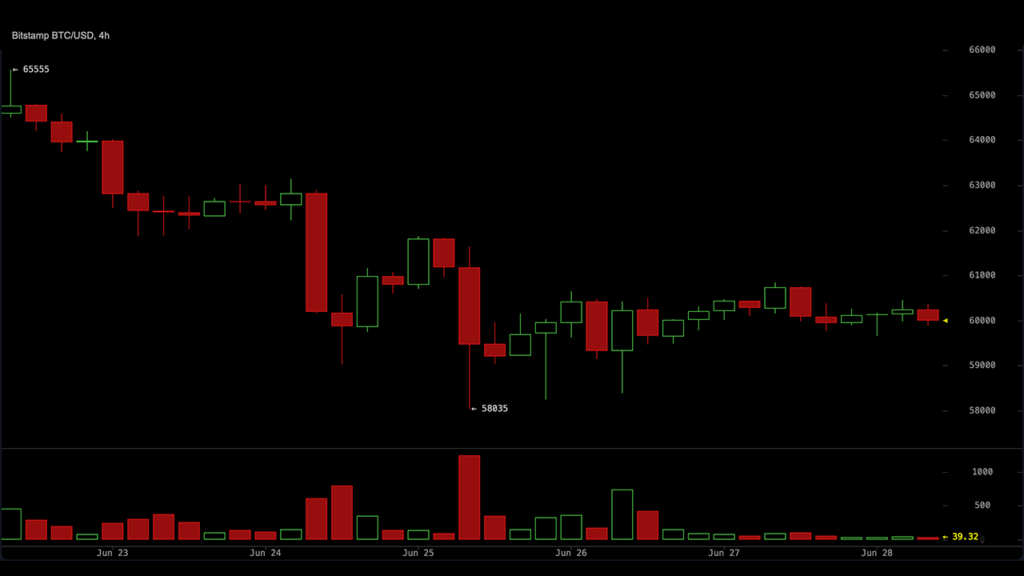

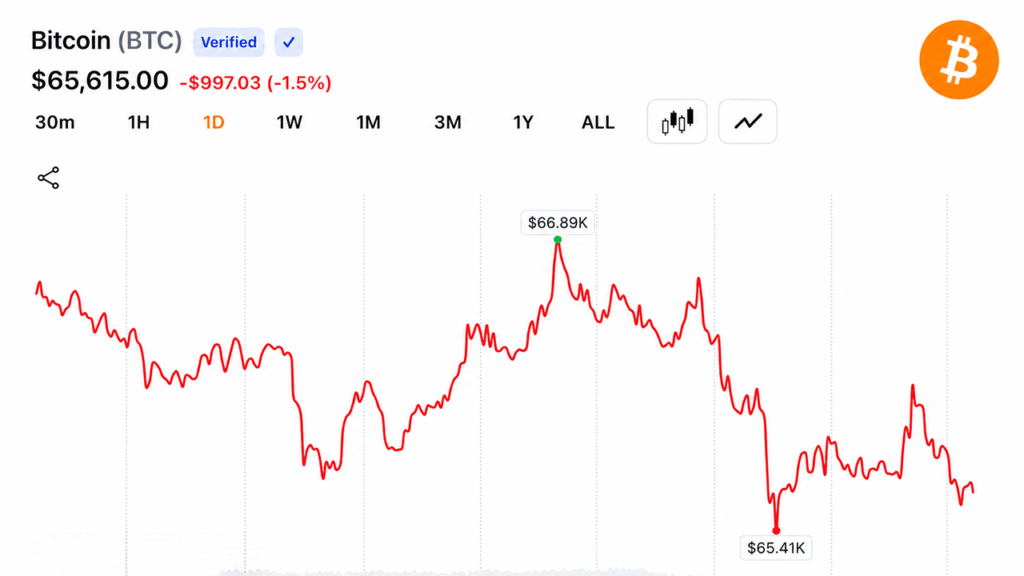

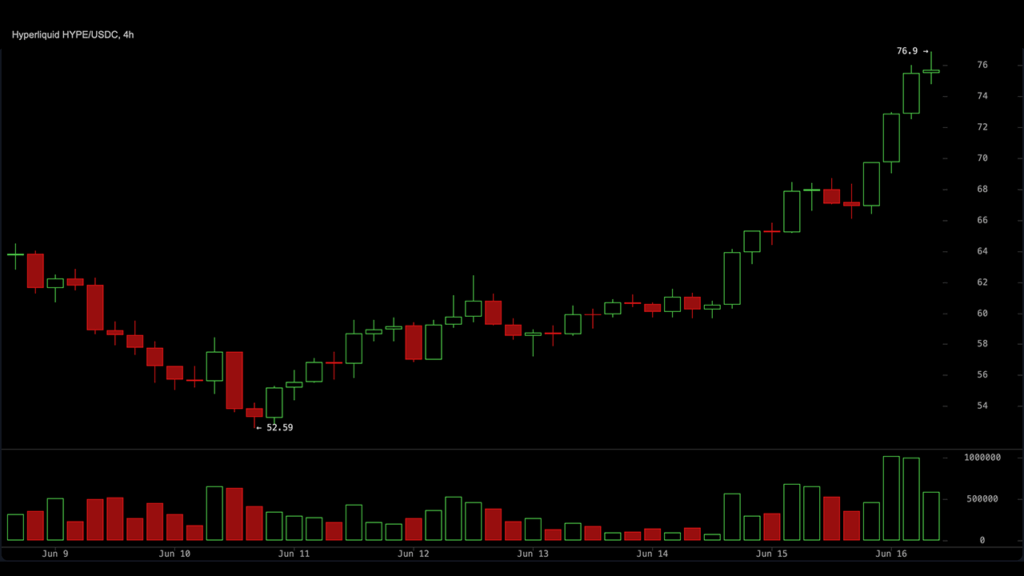

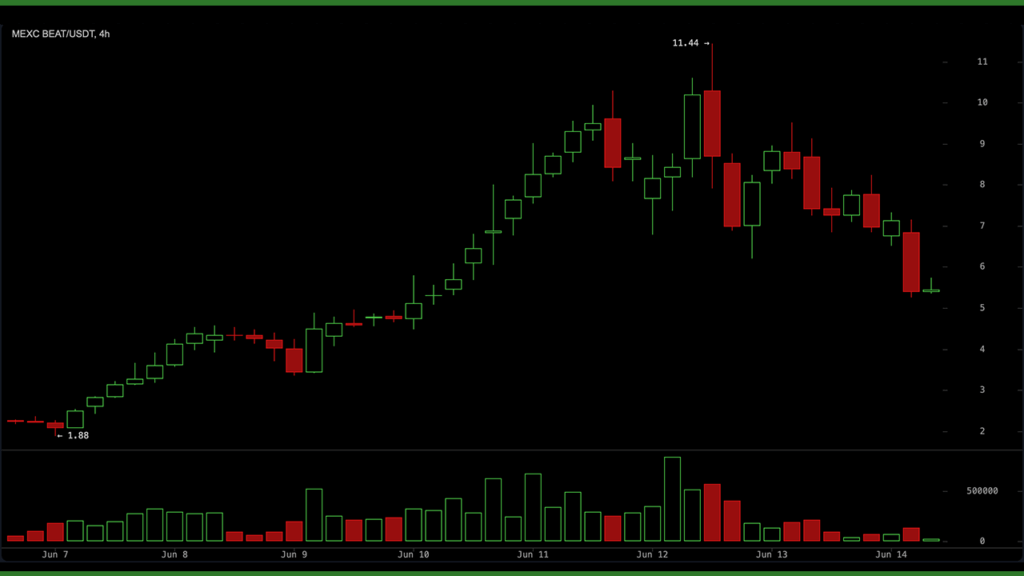

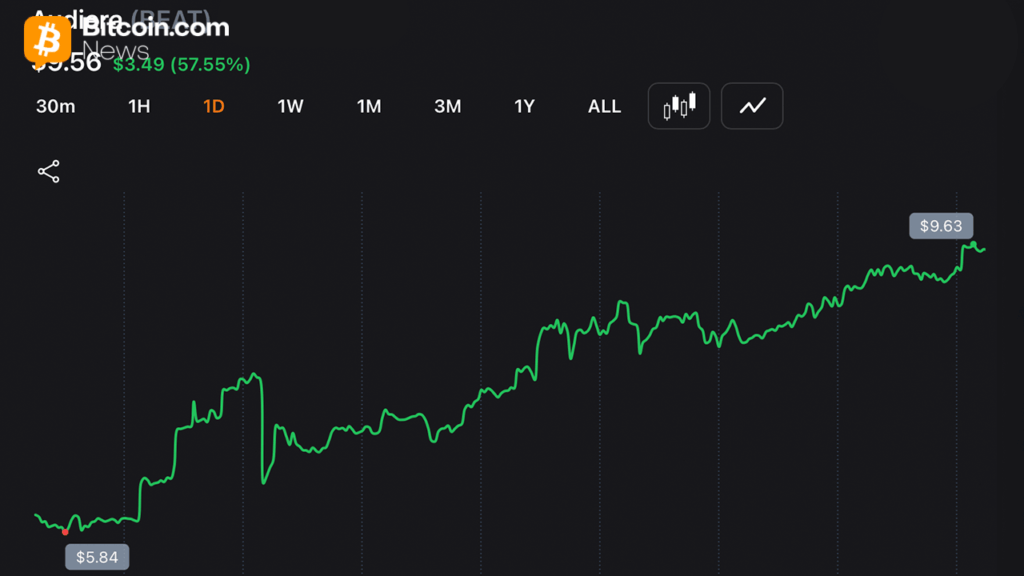

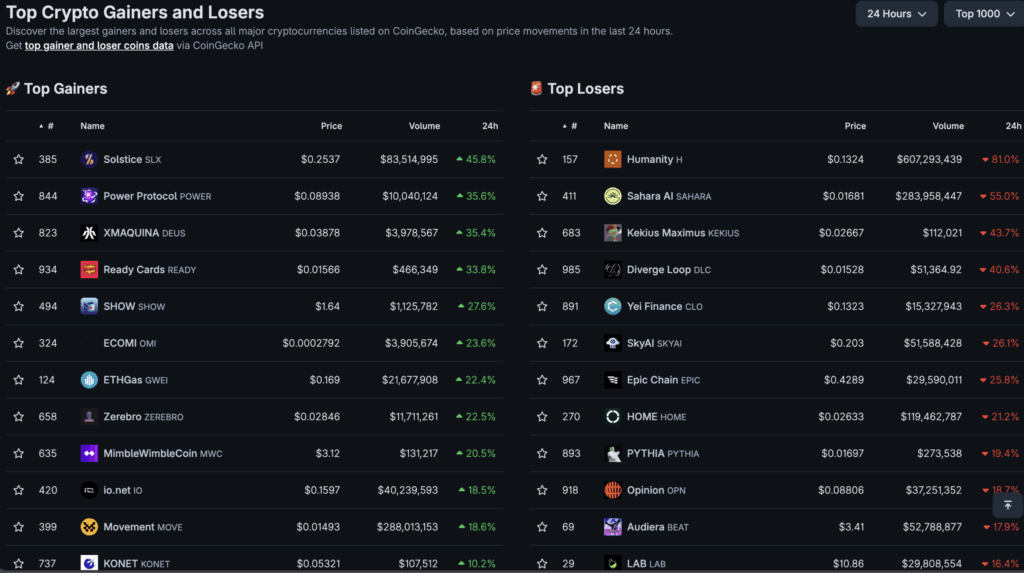

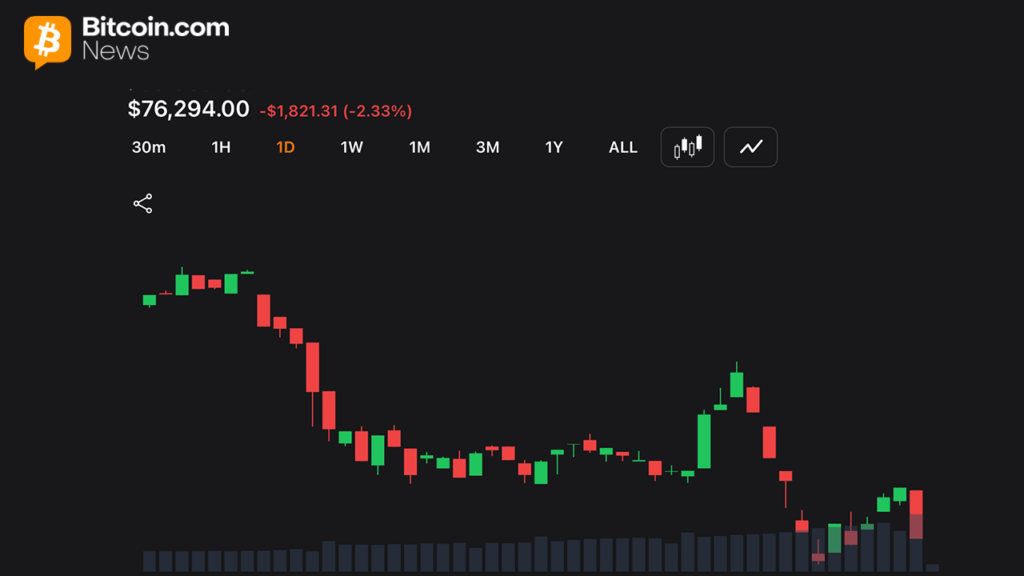

Robinhood Chain went live on July 1. CASHCAT deployed shortly after. Within roughly 24 hours it had rallied more than 1,700%, and over its first week it climbed more than 2,100%, reaching an all-time high above $0.17 and a market capitalization near $156 million, with some measurements putting the peak higher.

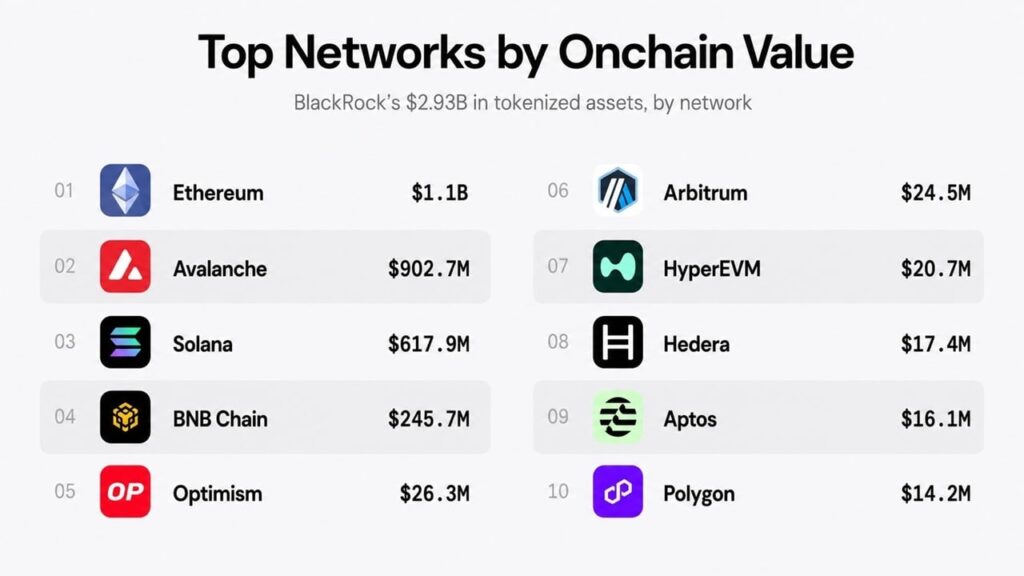

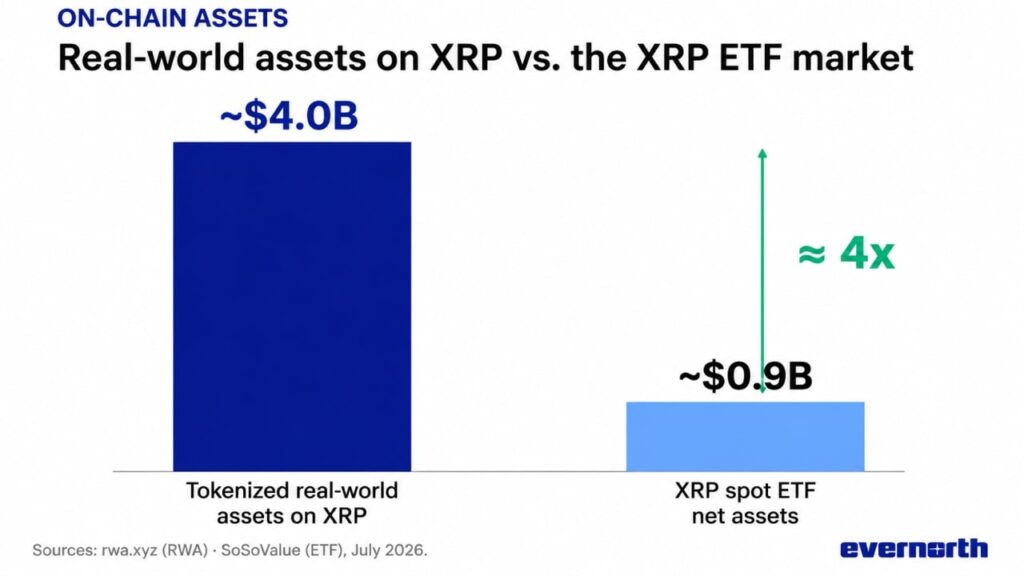

At its peak day on July 8, the token generated roughly $98 million in 24-hour volume, which was about 17% of the entire chain’s decentralized exchange volume. Set that against what the chain was built for: tokenized real-world assets on Robinhood Chain totalled roughly $12.8 million. At its high, one joke token was worth approximately twelve times every real asset on the network combined.

It did not stay alone. Cash Dog in Hood, Little John, Hoodrat, and Arrow followed within days, none of which existed before July 1. Noxa, the launchpad feeding the wave, was averaging roughly 18,600 new token launches per day. On July 8, Pump.fun added Robinhood Chain support, opening the chain to Solana’s memecoin crowd without bridging. For more context, crypto.news has covered the full story of the takeover.

Then it turned. On July 11, at the precise moment CASHCAT was hitting peak trading volume, Noxa stopped accepting new token launches. Two days later it went dark, citing concerns about low-quality tokens flooding the platform, having generated an estimated $12 million in cumulative fees. CASHCAT fell more than 33% in 24 hours. One prominent trader who claims to have ridden the token from a $10,000 market cap to $230 million dismissed the selloff as noise.

The Tenev problem

The CEO’s involvement is the reason this token is confusing rather than merely amusing, and the sequence matters.

On July 2, the day after the chain went live, Tenev told CNBC that the future of crypto is in real-world assets, drawing a line between productive tokenized assets and speculative tokens without underlying utility. His framing was that an asset not tied to an underlying utility is not a productive asset. It was a clean statement of the thesis the entire chain was built to prove, and it was, in effect, a dismissal of exactly the category CASHCAT belongs to.

Six days later, as CASHCAT climbed, he posted on X that while the company is building Robinhood Chain to be the best chain for real-world assets, it works great for memes too. He then followed the token’s account.

Both readings of that reversal are defensible. The charitable one: a permissionless chain cannot control what deploys on it, refusing to acknowledge the most visible thing on your own network would look ridiculous, and a light-hearted post is not an endorsement. Robinhood’s crypto chief stayed rigorously on message throughout, saying the company remains focused on building a secure and scalable foundation for real-world assets.

The uncharitable one: the follow and the post told the market what the company actually values, which is volume, and a retail buyer who sees the CEO engaging with a token named after his own company is going to draw a conclusion the disclaimer will not undo. The distinction between acknowledging and endorsing is clear to a lawyer and invisible to someone who just downloaded a wallet.

Who made money, and from whom

This is the part that gets celebrated and should be read carefully, because every one of these numbers has a counterparty.

One early buyer spent $838 and received 15.04 million tokens. They sold roughly 13.5 million for about $917,600 and held a remainder worth around $133,700, producing a return in the region of 1,250 times. A second wallet turned $85 into 17.4 million tokens and realized about $687,700 while sitting on roughly $1.2 million more on paper. The five most profitable wallets banked close to $3.7 million between them.

Now the other side. That $3.7 million came from the opposite end of roughly 12,300 sell orders. Every dollar of realized profit in a memecoin is a dollar someone else paid at a higher price, because the token produces no revenue and holds no assets. There is no external cash flow funding those returns. The gains are transfers.

The liquidity structure makes it worse than the market cap suggests. CASHCAT’s trading pool has been worth far less than the token’s headline capitalization, which means a $156 million number sits on a pool that cannot absorb anything close to $156 million of selling. Large trades swing price hard in both directions. A market capitalization is a multiplication, not a promise that the money is there.

And the standard verification does not exist. Security audits of the CASHCAT contract were not possible because Robinhood Chain is too new for the tooling to have caught up. That is a chain-wide condition, not a CASHCAT-specific failure, but it removes the check that would ordinarily flag a malicious contract before a nine-figure market cap forms on top of it.

How a memecoin actually prices

Because CASHCAT is the first token most Robinhood users will look at closely, it is worth walking exactly how a number like $156 million comes to exist, since almost nobody who quotes it understands what it measures.

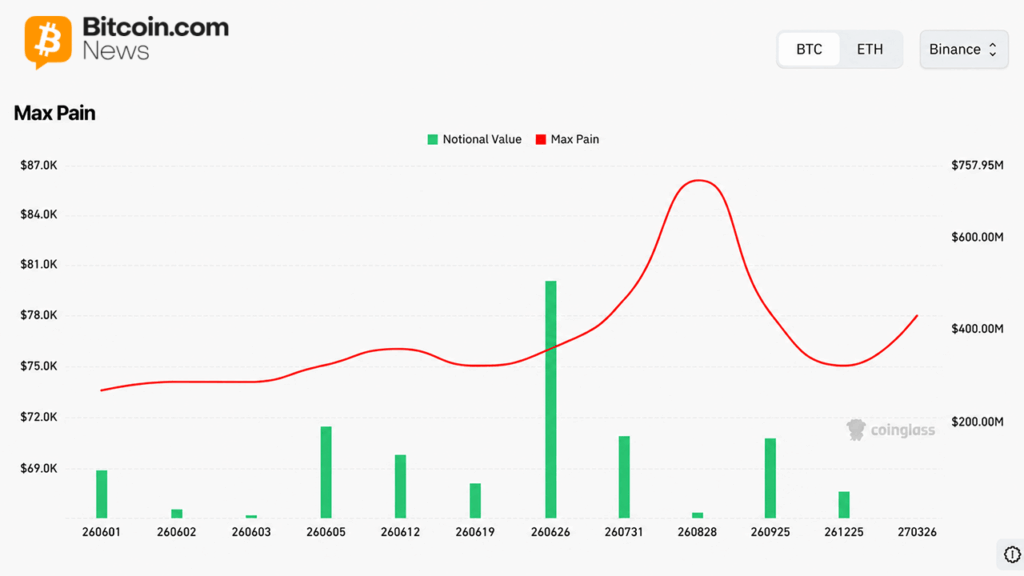

Market capitalization is a multiplication. Take the last traded price, multiply by circulating supply, print the result. CASHCAT has a fixed supply of one billion tokens, so at a price above $0.15 the arithmetic produces something in the region of $156 million. That is the whole calculation. It is not a valuation, not an appraisal, and not a statement that $156 million exists anywhere.

What makes the number misleading is where the price comes from. The last trade might have been for a few hundred dollars. In an automated market maker, price is set by the ratio of assets in a liquidity pool, and the pool behind CASHCAT has been worth far less than the token’s headline capitalization. So a relatively small purchase moves the ratio, moves the price, and instantly revalues all one billion tokens at the new level. That is why memecoins can add nine figures of notional value in a day: a thin pool is a lever, and modest buying at the margin repriced the entire supply.

The lever works identically in reverse, which is what July 13 showed. When Noxa exited and sentiment turned, sellers hit the same shallow pool and the price fell more than 33% in a day. Nothing about the token changed. Supply was still one billion. The contract was unaltered. The only thing that moved was the ratio in the pool, and the market cap followed it down mechanically.

This is why the comparison that ran through every headline, that CASHCAT was worth twelve times every real-world asset on the chain, is both true and slippery. It is true as arithmetic: $156 million against $12.8 million. It is slippery because the two numbers are not the same kind of thing. The tokenized asset figure represents real instruments with real backing that could be redeemed. The memecoin figure represents a price multiplied by a supply, sitting on a pool that could not absorb a fraction of it. One number is a balance. The other is an echo.

The practical implication for anyone holding: your position is worth the market cap right up until you try to sell, at which point it is worth whatever the pool gives you. In a token where five wallets extracted roughly $3.7 million against 12,300 sell orders, the people who found out first were the ones who tried. That is why thin liquidity moves price so hard.

What this token actually shows

Set the price action aside and CASHCAT is the cleanest available case study in how new chains actually bootstrap, which is why it is worth understanding even if you would never touch it.

The optimistic reading, which serious traders make: memecoins are the ignition sequence. A new chain needs transactions, wallets, and liquidity to look alive, and speculation delivers all three faster than tokenized Treasuries do. Solana grew through a memecoin cycle before producing serious infrastructure, and one veteran trader explicitly compared Robinhood Chain’s early ecosystem to Solana’s. The automated market makers, oracles, and routing built to service speculation are the same rails that tokenized equities will eventually need. In that reading CASHCAT is not a distraction from the strategy; it is the first stage of it. That in the category CASHCAT belongs to.

The pessimistic reading, which the timeline supports: memecoin traders are mercenary by construction, loyal to activity rather than to any chain, and the moment a flashier venue offers quicker returns the volume leaves and the $12.8 million of tokenized assets is what remains. The launchpad that produced the entire boom extracted $12 million in fees and exited within eleven days of the chain going live. That is not the profile of a bootstrapping sequence. It is the profile of an extraction cycle, and the 33% drop when the launchpad left is the evidence.

Which reading is right gets settled by a single number, and it is not CASHCAT’s price. It is whether tokenized real-world assets on Robinhood Chain grow well beyond roughly $13 million while the speculation fades. Robinhood’s second-quarter earnings on July 29 are the first real look. Until then, CASHCAT is a token named after a discarded company name, worth more than everything the chain was built to carry, running on an unaudited contract, on a network whose CEO spent one week explaining why assets like it do not last and the next week noting they work great anyway.

What to watch

If you are tracking this token instead of trading it, three things carry information.

Whether the ecosystem keeps spawning. STONKCAT opened a $SCAT presale on July 16, and a MemeToro presale is running alongside it, both borrowing Robinhood Chain’s branding and pitching future products. New entrants arriving weeks after the launchpad that started the wave exited tells you the branding gap is now a repeatable business, which is bearish for CASHCAT specifically: every new token competes for the same attention that is the only thing holding its price up. It also shows how launchpads mint tokens on demand.

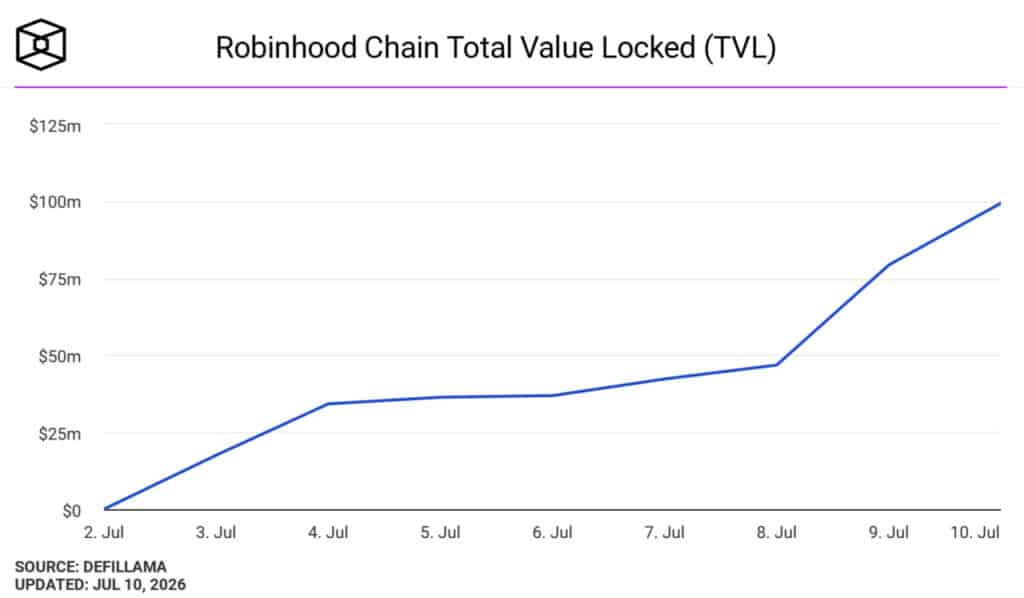

Whether the chain’s real assets grow. Tokenized real-world assets on Robinhood Chain sit around $12.8 million against roughly $312 million in total value locked. That figure, not CASHCAT’s price, decides whether the memecoin wave was an ignition sequence or an extraction cycle. Robinhood’s second-quarter earnings on July 29 are the first look at Stock Token adoption from the company’s own books.

Whether liquidity deepens or thins. The pool behind CASHCAT has been worth far less than the token’s headline capitalization, which is the mechanism behind both the rise and the 33% single-day fall. A token whose pool deepens is a token that can absorb selling. A token whose pool thins as attention rotates is a token whose market cap becomes progressively more theoretical. Also relevant: Robinhood Chain’s 90-day gas subsidy has been making trading artificially cheap, and its expiry is a real test.

The broader point for anyone reading this as a lesson instead of a trade: CASHCAT did nothing unusual. It is a well-executed example of an entirely standard pattern, distinguished only by the quality of its joke and the fact that a public company’s CEO engaged with it. The pattern will repeat on the next chain, with a different name, and the mechanics will be identical. What makes this instance worth remembering is the setting. Most memecoins erupt on chains built by anonymous developers for exactly this kind of activity, where nobody claims to be surprised. CASHCAT erupted on a network built by a listed American brokerage, marketed to institutions, staffed with compliance officers, and launched with a keynote about the future of finance. It took six days for the joke to become the chain’s largest asset by market capitalization, and the company could do nothing about it, because permissionless means permissionless. That is the lesson worth carrying: a corporate chain cannot choose its users any more than a public square can. Robinhood built the venue and the crowd decided what it was for.

Frequently asked questions

What is CASHCAT?

A community memecoin on Robinhood Chain, the Ethereum layer 2 Robinhood launched on July 1, 2026. It has a fixed supply of one billion tokens and a contract address of 0x020bfC650A365f8BB26819deAAbF3E21291018b4. It has no product, no utility, and no affiliation with Robinhood. Its own website describes the project as fan fiction with a ticker and says the utility is cat.

Is CASHCAT affiliated with Robinhood?

No. It is not owned, endorsed, backed, or listed by Robinhood Markets, and the token’s own website disclaims any connection to the company or to Vlad Tenev. The name references CashCat, the working name Tenev and co-founder Baiju Bhatt used before the company became Robinhood, a detail preserved in a New Yorker profile. That is trivia, not a relationship.

Why did CASHCAT rise so fast?

A combination of legible lore and a new chain with nothing else on it. The name connected instantly to Robinhood’s founding story, Robinhood Chain had just launched with cheap fees and easy token creation, and attention concentrated on the first breakout token. It rallied more than 1,700% in 24 hours and more than 2,100% over its first week, reaching a market cap near $156 million.

Did Vlad Tenev endorse CASHCAT?

Not formally. On July 2 he told CNBC that assets not tied to an underlying utility are not productive assets. On July 8, as the token climbed, he posted that while the company is building the chain for real-world assets, it works great for memes too, and he followed the token’s account. That is acknowledgement rather than endorsement, but the distinction is clearer to a lawyer than to a retail buyer.

How much was CASHCAT worth compared to the chain’s real assets?

At its peak, roughly twelve times more. Tokenized real-world assets on Robinhood Chain total around $12.8 million, while CASHCAT reached a market capitalization near $156 million. On its biggest day the token generated approximately $98 million in 24-hour volume, about 17% of the entire chain’s decentralized exchange volume.

Why did CASHCAT crash?

Noxa, the launchpad driving the chain’s memecoin wave, stopped accepting new launches on July 11 as CASHCAT hit peak volume, then went dark two days later, citing low-quality tokens flooding the platform. It had generated an estimated $12 million in cumulative fees. CASHCAT fell more than 33% in 24 hours following the exit.

Who made money on CASHCAT?

A small number of early wallets. One turned $838 into roughly $1.05 million across realized and unrealized value, about 1,250 times. Another turned $85 into roughly $687,700 realized plus $1.2 million on paper. The five most profitable wallets took close to $3.7 million between them. That money came from the other side of roughly 12,300 sell orders, since a memecoin produces no revenue and gains are transfers between participants.

What are the risks?

Considerable. The trading pool is worth far less than the headline market capitalization, so large trades swing price sharply and the stated value cannot be exited at that value. Security audits of the contract were not possible because Robinhood Chain is too new for verification tooling. The token has no revenue, no assets, and no utility, so price depends entirely on attention, which has already proven it can leave in a day.

Disclaimer: This article is for information and educational purposes only and does not constitute financial or investment advice. Memecoins are extremely speculative, frequently trade on thin liquidity, and most participants lose money. Contract addresses and project claims should be verified independently before any transaction. Nothing here is a recommendation to buy any token. Always do your own research. Figures are accurate as of July 17, 2026 and move rapidly.